Streamlining ESG Reporting Requirements

The Corporate Sustainability Reporting Directive (CSRD) is intended to reallocate capital flows towards sustainable investments. However, previous research by the TRR 266 Accounting for Transparency has shown that regulation can sometimes be counterproductive, as resources are diverted from real sustainability projects to pure reporting. To ensure the competitiveness of companies, regulators should therefore streamline current reporting requirements and reduce bureaucracy in a targeted manner. Our research provides clarity in the regulatory environment and delivers data-driven insights for business and political decision-making processes. We analyze which areas of sustainability reporting are overly bureaucratic, how this affects business decisions, and what regulators can do to improve the CSRD.

Companies call for reducing bureaucracy

The increasing requirements for sustainability reporting present major challenges for companies in Europe. Small and medium-sized enterprises (SMEs) complain about the burden of the numerous reporting obligations and highly complex requirements. Politicians have now recognized this. The EU Commission announced the so-called “Omnibus” law in November 2024, which aims to reduce reporting requirements for CSRD, CSDDD, and EU taxonomy by at least 25 percent, for SMEs by up to 35 percent – with the goal of reducing bureaucracy and providing noticeable relief for SMEs. Specific improvement measures include exempting companies with fewer than 1,000 employees from the reporting requirement. This would apply to 80 percent of the companies previously obligated to report. For other companies, the reporting requirement will be postponed by two years. The law thus responds to the increasingly negative perception of reporting requirements: 67.6 percent of companies in Germany now view the CSRD negatively, primarily due to its complexity (60.4 percent) and high cost (56.4 percent).

But which specific reporting requirements contribute most to the bureaucratic burden, and in which processes does bureaucracy arise in the context of sustainability reporting? Which companies are particularly affected, and how does bureaucracy influence business decisions?

Data from the German Business Panel provides insight into these questions:

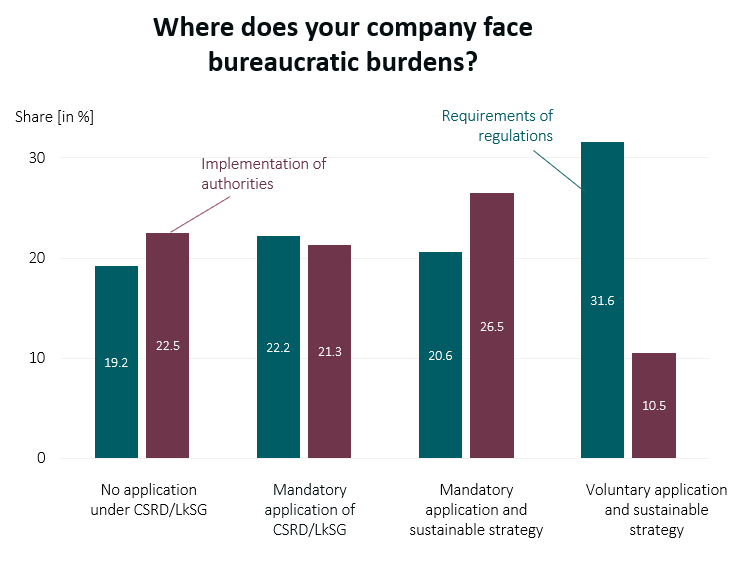

In which areas does bureaucracy exist?

Companies perceive the documentation requirements along supply chains as particularly challenging, with approximately one-third (34.3 percent) identifying them as a major burden. Additionally, one in five companies (20.4 percent) regard the preparation of sustainability reports under CSRD/ESRS as bureaucratic. Other contributing factors include the requirements for report digitization and compliance with the EU taxonomy.

The sources of bureaucracy in sustainability reporting can be categorized into two aspects: first, the substance of legal regulations (such as detailed disclosure and documentation criteria), and second, the interaction with regulatory authorities. Companies without their own sustainability reporting more frequently attribute the burden to bureaucratic dealings with authorities, whereas those who report voluntarily see the main source of burden in the regulations themselves.

Which companies are particularly affected?

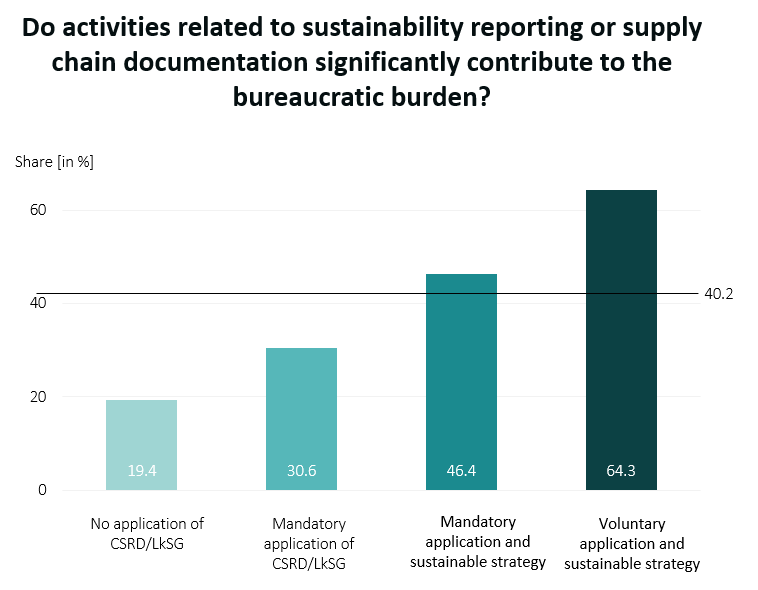

The perception of bureaucratic burden is not equally pronounced across all companies. Complaints are most frequent among voluntary users of sustainability reporting who also pursue a sustainable corporate strategy. Here, 64.3 percent of companies consider the reporting requirements to be overly bureaucratic. The burden is also noticeable for companies that are subject to mandatory reporting under the CSRD or the Supply Chain Due Diligence Act (LkSG), especially when ESG metrics are also used internally for corporate management. It is striking that even companies without direct reporting obligations sometimes complain about bureaucracy because they have to pass on information to customers or suppliers. In addition, small and medium-sized enterprises are often particularly burdened because they do not have the resources and expertise to implement ESG requirements efficiently.

Significant consequences for investments

The impact on economic decisions is significant, with over half of companies (54.1 percent) postponing planned investments because of the bureaucratic burden. Nearly 41 percent have postponed new product developments, 39 percent have abandoned foreign business relationships, and 28 percent have relocated projects abroad. Companies that perceive the CSRD as a burden are particularly affected: here, the proportion of investments not implemented rose to as much as 60 percent. This makes it clear that reporting requirements not only take up considerable human and financial resources, but also have a negative impact on business decisions relating to innovation and growth. Bureaucracy in sustainability reporting can thus inadvertently slow down the actual goals – greater sustainability and competitiveness.

Related Report:

Contact the German Business Panel:

The Sustainability Reporting Navigator

The Sustainability Reporting Navigator (SRN) is a free, open-science platform aiming to contribute neutral, evidence-based insights to current policy debates about European sustainability reporting. Via a public repository, the SRN facilitates easy access to more than 800 CSRD reports, which can be explored with the help of an AI assistant. Users can further benchmark companies’ sustainability reporting in a customized dashboard and stay up to date with current reporting requirements via the SRN Academy.

Interview with the researchers behind the Sustainability Reporting Navigator:

Research findings from the Sustainability Reporting Navigator

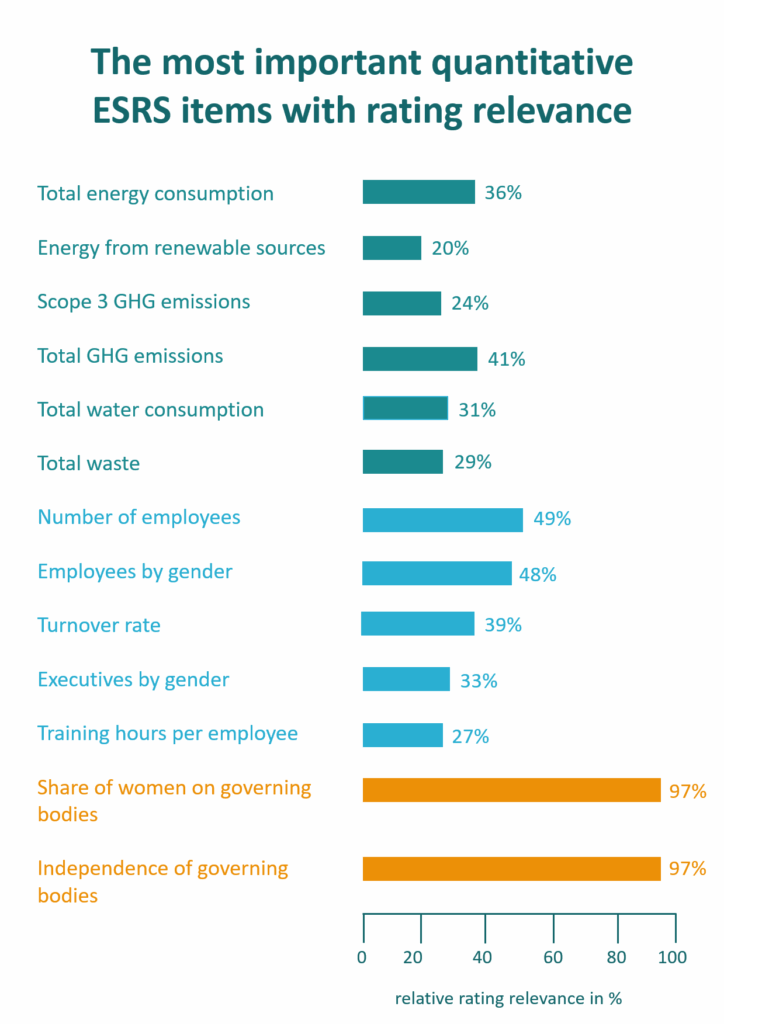

Only 10 percent of quantitative ESRS data points relevant for ESG ratings

While Brussels wants to set an example for greater ESG transparency with the ESRS, NGOs criticize the standards as being too soft. Practitioners, on the other hand, warn of a “data graveyard” and high implementation costs. This is because many companies do not yet know which of the numerous new disclosures are really relevant for stakeholders and the capital market – and should therefore be prioritized.

The ESRS comprises a total of over 1,100 data points, 283 of which are quantitative. A study from 2023 examined which of these are actually included in ESG ratings and thus form the basis for investor decisions. The result: only around 10 percent of quantitative ESRS data is relevant for ratings. But this 10 percent carries weight – it accounts for 62 percent of the E&S data used in ratings. Among the top data points are, for example, the proportion of women in the workforce and greenhouse gas emissions – information that is not only required by regulation but also highly relevant to investors.

For companies, these “core data points” provide initial guidance for implementing the ESRS: knowing what rating agencies use allows companies to set priorities for data collection. Nevertheless, the obligation to conduct a comprehensive materiality assessment remains—not only from an investor perspective, but also in relation to society and politics.

The analysis also shows that even large DAX companies have so far only disclosed around 50 percent of the data points relevant for ratings. The rates are even lower for smaller companies in the MDAX and SDAX. This highlights a considerable need to catch up in order to meet both the requirements of the ESRS and the expectations of the capital market.

The overlap between ESRS and ESG ratings is therefore smaller than hoped for – but where it does exist, it is all the more relevant. For companies, this means targeted implementation rather than blind compliance. And for the capital market, it means an opportunity to close the gap between regulatory transparency and financial relevance.

Read the publication:

EFRAG amendment: existing data points reduced, but new ones added

Sustainability reporting requirements under the Corporate Sustainability Reporting Directive (CSRD) continue to evolve. In 2025, EFRAG issued revisions to the European Sustainability Reporting Standards (ESRS) with the stated objective of simplifying disclosure requirements and reducing the reporting burden for companies. These adjustments are intended to make sustainability reporting more proportionate.

To analyze the practical implications of these revisions, the SRN team conducted a large-scale review of CSRD reports. Their analysis combines information on more than 700 companies’ 2024 disclosures with detailed information on the revisions at the datapoint level. The findings indicate a substantial streamlining of mandatory datapoints. Overall, the volume of required datapoints has been roughly cut in half, with reductions being most pronounced for qualitative datapoints.

However, the revisions do not merely eliminate content. A considerable share of the remaining datapoints has been newly introduced or amended. As a result, while companies face fewer reporting obligations in aggregate, they must adapt existing systems, processes, and internal controls to align with updated definitions, structures, and expectations.The analysis further shows that the reduction in datapoints is broad in scope and consistent across industries, regions, or company sizes.

The annotated datapoint list is available on the SRN website, together with further resources centering facilitating companies’ CSRD reporting and benchmarking.

Contact the researcher team of the Sustainability Reporting Navigator:

Technical support & digitization necessary

In addition, technical support and digitalization are crucial to making the reporting process efficient. Collecting around 1,100 data points in accordance with the ESRS requires powerful IT structures, which is why specialized software solutions such as ESG management systems or automated reporting tools are becoming increasingly important. They could simplify reporting processes and make them scalable, also from the perspective of the authorities. Against this backdrop, it is clear that political relief measures, technological solutions, and scientific support are equally necessary to make reporting requirements more practicable—especially for SMEs, which often have limited personnel and technical resources.

Support for companies from SRN Academy: Free course on emissions reporting (ESRS 1)

The SRN not only offers research data and analyses, but also supports companies through practice-oriented knowledge transfer. Take part in the free course on emissions reporting (ESRS 1) and demonstrate your knowledge of reporting by successfully analyzing the sustainability reports of three companies.