How Effective Are ESG Reporting Requirements?

Disclosure rules are designed not only to boost transparency and improve decision-making but also to push companies toward more sustainable practices – socially and environmentally. But do they live up to that promise? Do companies truly change their behavior under regulatory pressure? And what effects and unintended consequences might arise along the way? Researchers at TRR 266 are diving into these critical questions.

Are Companies Becoming More Sustainable?

Do companies change their behavior when required to disclose how they treat employees or how vulnerable they are to climate risks? Are they truly becoming more socially and environmentally responsible? Studies reveal the real impact of social and environmental reporting mandates — and expose where these rules fall short.

Social Metrics Under Scrutiny: What Mandatory ESG Reporting Can Really Achieve

From fair working conditions and workplace safety to training opportunities — social sustainability has become a competitive factor, especially in an era of skilled labor shortages. Transparent reporting on how responsibly companies treat their employees matters — to job seekers, investors, and a growing range of stakeholders. But does mandatory reporting actually lead companies to improve their social standards? A recent study provides answers. It examines how mandatory social sustainability reporting affects corporate practices and financial performance.

The study shows: mandatory social sustainability reporting drives change. European companies reporting under the Non-Financial Reporting Directive (NFRD) have significantly improved their working conditions – outpacing their U.S. counterparts, who face no such requirements. These improvements also come with financial gains.

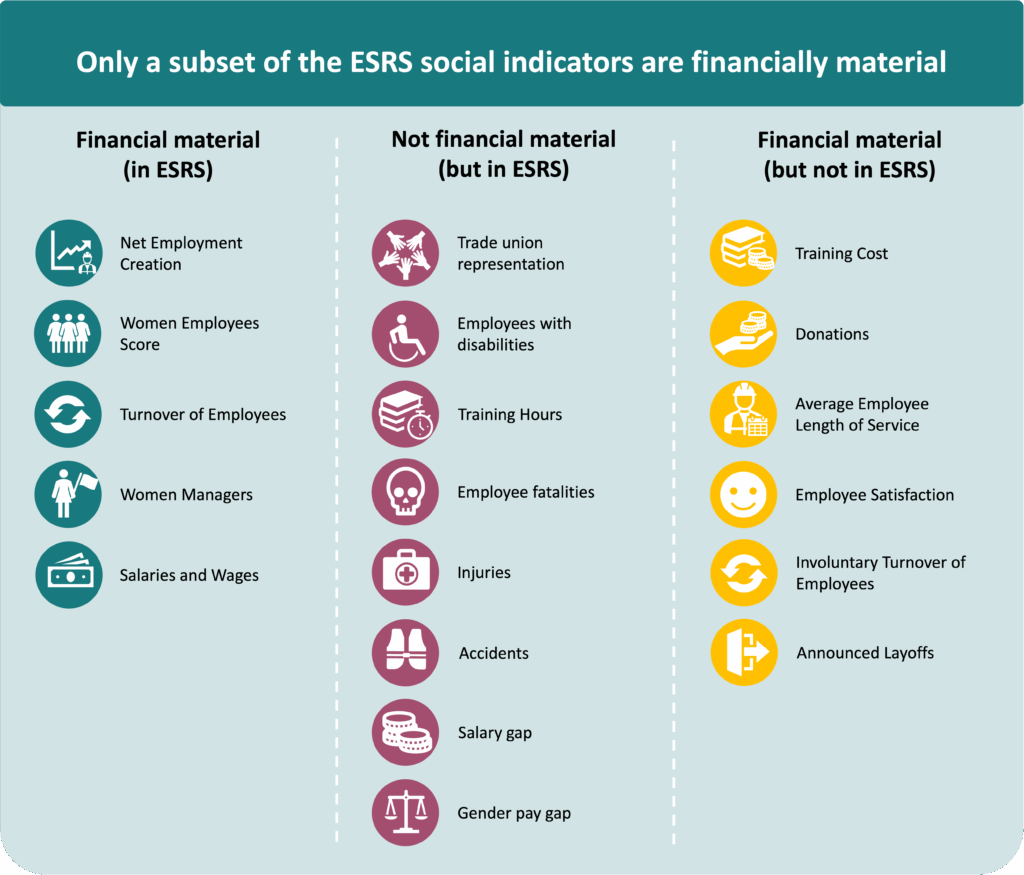

The study goes further by evaluating which specific social indicators actually matter for a company’s financial performance, based on sustainability information published by European companies between 2013 and 2020. Building on these findings, the study identifies the social indicators most likely to be relevant under the new European Sustainability Reporting Standards (ESRS). These binding reporting standards have been gradually introduced since 2024 as part of the Corporate Sustainability Reporting Directive (CSRD), replacing the NFRD.

The results are mixed: Only a subset of the ESRS social indicators show strong links to business success. Metrics such as the share of female employee and managers, employee turnover, as well as salaries and wages are clearly tied to financial performance. Others – including the gender pay gap, trade union representation, or employee fatalities – show little or no correlation. Meanwhile, key metrics like employee satisfaction, involuntary employee turnover, or total donations are not yet part of the ESRS reporting mandate, despite being strongly tied to a company’s financial performance.

Guidance for Regulators

The message to regulators is clear: To craft smarter and effective reporting requirements, empirical evidence should guide the selection of metrics. A bloated catalogue of KPIs risks diluting the impact of ESG disclosures. The financial relevance of the metrics is key to strengthening the legitimacy and acceptance of reporting requirements – especially among capital market participants.

Read the study:

Contact the researchers:

How ESG Reporting Is Shaping Corporate Decision-Making

Mandatory sustainability reporting is rapidly gaining ground, significantly influencing both the strategic and operational choices companies make. The new Corporate Sustainability Reporting Directive (CSRD) presents opportunities for more sustainable business management but also introduces considerable challenges — including increased documentation demands, revamped reporting processes, and a host of fresh regulatory requirements. Recent studies shed light on how companies are adapting to these evolving standards and reveal the impact on investment decisions, innovations, and long-term strategic planning.

Bureaucracy Stifles Investment: Current Data on the Impact of the CSRD

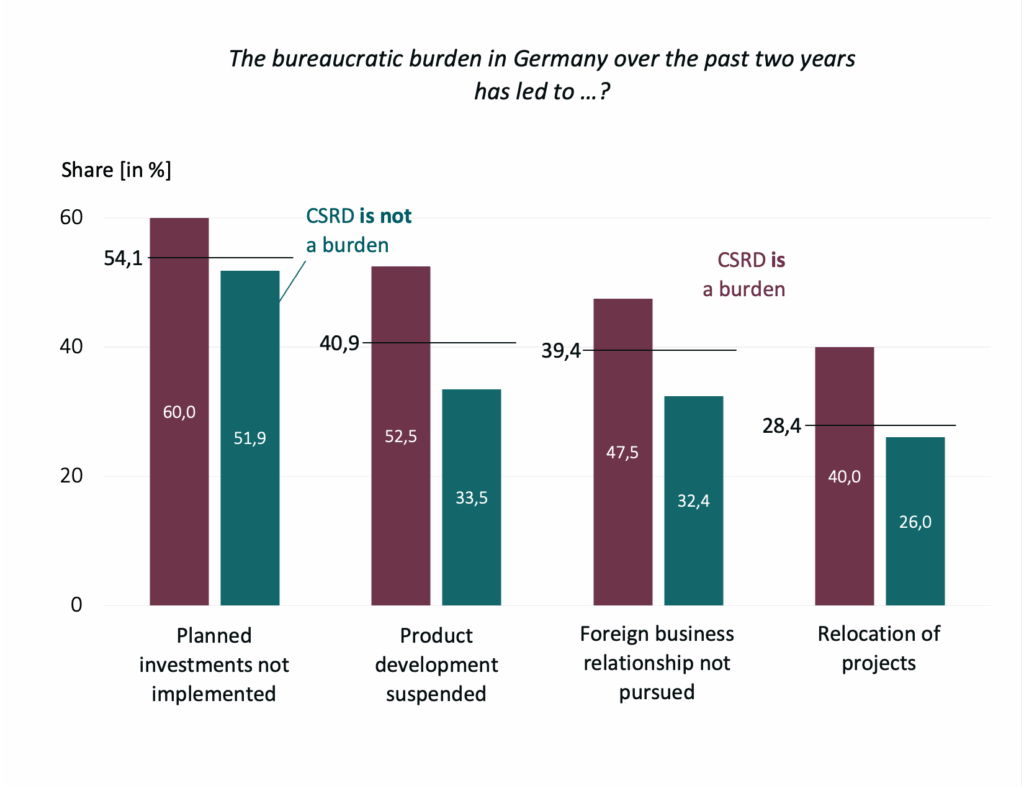

New sustainability reporting requirements are imposing substantial bureaucratic burdens on many companies — with noticeable economic consequences. According to an analysis by the German Business Panel, more than half of firms (54.1%) have cancelled planned investments over the past two years due to bureaucratic burden. Among companies that report bureaucratic strain in connection with the CSRD, the number rises to 60%.

Particularly challenging for businesses are the documentation requirements along supply chains (34.3%) and the preparation of sustainability reports (20.4%). Surprisingly, companies that report voluntarily and actively use ESG data for management purposes perceive the bureaucratic burden most strongly. Around 64% of these “voluntary adopters” complain about excessive administrative effort – often small and medium-sized firms with limited resources.

It is not only the content of the regulations that causes frustration — interactions with authorities are also frequently cited as drivers of bureaucracy. The intended shift toward greater sustainability may thus be slowed: instead of fostering innovation and transformation, many companies experience the new ESG mandates as an obstacle – leading to postponed projects, budget cuts, or even offshoring.

When bureaucracy prevents investment, sustainability policy fails to achieve its goal. It remains to be seen what impact the newly introduced ‘omnibus’ law will have, which aims to reduce reporting and disclosure obligations by at least 25 percent.

Read the report:

Contact the reseachers:

How does ESG reporting affect the organizational design of firms?

ESG reporting requirements do not only influence investment and other business decisions, they also affect how firms organize themselves internally. In response to EU reporting rules such as the Non-Financial Reporting Directive (NFRD), many companies are adjusting how sustainability responsibilities are assigned within their organizations. So what kinds of organizational change can mandatory reporting trigger, and does it have potential side effects?

Beyond Disclosure: How Firms Reshape Organizational Design in Response to the NFRD

This study examines how firms adjust their established sustainability responsibilities within their organization in response to the NFRD. The researchers distinguish between two structural changes:

- specialization, where sustainability responsibilities are assigned to dedicated roles (such as a Chief Sustainability Officer or a Head of Corporate Sustainability) or formal bodies (such as sustainability committees),

- and generalization, where these responsibilities are embedded in existing managerial functions, such as finance or operations.

Using CDP survey data, the study finds that, on average, firms respond to the NFRD by generalizing sustainability responsibilities and integrating them into existing managerial roles rather than creating dedicated sustainability positions. This effect is mainly driven by the additional reporting requirements introduced by the NFRD, rather than by low sustainability performance before the regulation came into effect.

The study also provides insights into the consequences of generalizing versus specializing sustainability responsibilities. Firms that specialize experience a significant decline in sustainability reporting quality after the NFRD is introduced. In contrast, firms that generalize achieve short-term improvements in sustainability performance. However, firms that specialize show stronger long-term improvements in sustainability performance. These findings indicate that while generalization can deliver faster performance gains, it may be less effective in supporting long-term sustainability improvements.

In terms of financial outcomes, firms that generalize experience declines in both short- and long-term return on assets, as well as a long-term decline in market valuation. These results indicate that generalization comes with additional costs, as managers responsible for both financial and sustainability goals may face competing demands. The researchers suggest that these negative financial effects may be linked to incomplete organizational adjustments, as firms change responsibility structures without fully adapting incentive systems and performance monitoring mechanisms.

Recommendations for Regulation and Policy:

The findings show that sustainability reporting regulation can trigger meaningful organizational change, but may also lead to unintended financial consequences. Regulators aiming to improve long-term sustainability outcomes may need to complement reporting mandates with policies that encourage a more comprehensive integration of sustainability into management control systems, rather than relying on transparency alone.

Read the study:

Contact the researchers:

How ESG Reporting Requirements Are Reshaping Corporate Financial Disclosure

ESG reporting obligations do more than dictate which social, environmental, and governance information companies must disclose — they are also transforming how businesses communicate overall. Notably, these mandates have a significant impact on financial reporting and other forms of corporate reporting.

Financial Reporting in Flux: How ESG Is Changing What Companies Report

With the introduction of mandatory sustainability reporting, ESG can reshape not just what companies disclose about social, environmental, and governance issues — but also how they report their financial performance. A international study finds that firms, on average, strategically adjust their voluntary financial disclosures when required to report ESG metrics.

On average, after new regulations take effect, companies tend to issue traditional earnings guidance less frequently and instead provide more non-earnings forecasts, such as revenue projections, capital expenditure forecasts, or cash flow guidance. This shift moves the focus away from pure profit metrics to a broader set of financial metrics that better align with nonfinancial disclosures. This, in turn, suggests that firms are responding to a shift in the information needs of capital markets – and the demands of their stakeholders for consistent reporting that connects financial and non-financial information.

Whether a company actually adapts its financial reporting depends largely on its individual disclosure incentives. Firms facing high pressure from stakeholders – such as analysts or institutional investors – tend not to cut back on earnings forecasts, since the pressure to report is too high. Instead, they expand their non-earnings projections more extensively. In markets with low competitive pressure, companies typically expand their non-earnings forecasts more than those in highly competitive markets, as the economic risk of disclosing sensitive information is potentially lower. Interestingly, companies that voluntarily disclosed ESG data prior to the new rules hardly change their behavior.

Guidance for Regulators

Notably, mandates focused on environmental disclosures drive the most significant adjustments, while social and governance reporting has less impact. The study offers valuable insights for regulators and standard setters: companies are already striving to better integrate financial and nonfinancial reporting on their own, preserving transparency and relevance for stakeholders. This suggests that a mandatory integration of nonfinancial information into financial reports may not be strictly necessary.

Read the study:

Contact the researchers: