Targeted Transparency: Nudging Firms towards changing their Business Activities in Socially Desirable Ways

Nudging is a popular concept from behavioral economics that has also found its way into other (research) fields. With nudging positive reinforcement and indirect suggestions are used as ways to influence the behavior and decision making of groups and individuals. A classic example is that in order to help your employees make healthy food choices you could replace the jar with sweets at the reception desk with a bowl of fruit, therewith giving the employees a small push, a nudge, in the right (healthy) direction. As such, nudging is said to be an alternative way to achieve compliance, contrasting formal methods such as legislation. However, nudging and formal regulations can also go hand in hand. Katharina Hombach and Thorsten Sellhorn published a review on ‘targeted transparency’, which is transparency regulation aimed at nudging firms towards changing their business activities in socially desirable ways. They developed a framework that lays out the necessary conditions under which targeted transparency regulation can be effective and reviewed the emerging empirical evidence. They discuss their framework and main findings below.

Targeted transparency regulation’s objectives extend beyond pricing. These regulations force companies or agencies to disclose information in standardized formats to reduce specific risks, account for negative externalities, or to improve provision of public goods and services. Mandatory nutrition labeling of food products, intended to reduce unhealthy eating habits and therewith potentially large health costs to individuals and society at large, is an example of such a policy. However, targeted transparency may also address environmental, equality and various other issues. We looked at a specific type of targeted transparency: targeted transparency implemented by securities regulators. These mandated disclosures are aimed not only at providing decision-useful information to investors, but also at mobilizing pressure from a broad range of potential users, including consumers, employees, citizens, the media as well as NGOs and other advocacy groups. Examples include CSR reporting, country-by-country reporting of oil and gas firms’ payments to governments, and disclosure of the gender composition of corporate boards. We specifically looked at studies on recent CSR reporting requirements in the E.U. and Specialized Disclosure regulation in the US. Although these disclosure requirements are implemented via corporate disclosure regulation, they are primarily aimed at fostering public policy objectives that are at least partly unrelated to securities regulators’ traditional objectives and mandates. For example, the EU’s CSR Directive intends to foster outcomes related to firms’ environmental impact, social and employee aspects, human-rights and anti-corruption measures, and board diversity, all elements that do not directly relate to pricing and the capital market. We developed a framework showing that in order to create an effective nudge, targeted transparency regulation needs to set off a causal chain that links the disclosure requirement to the targeted corporate action.

Necessary conditions for effective targeted transparency regulation: a framework

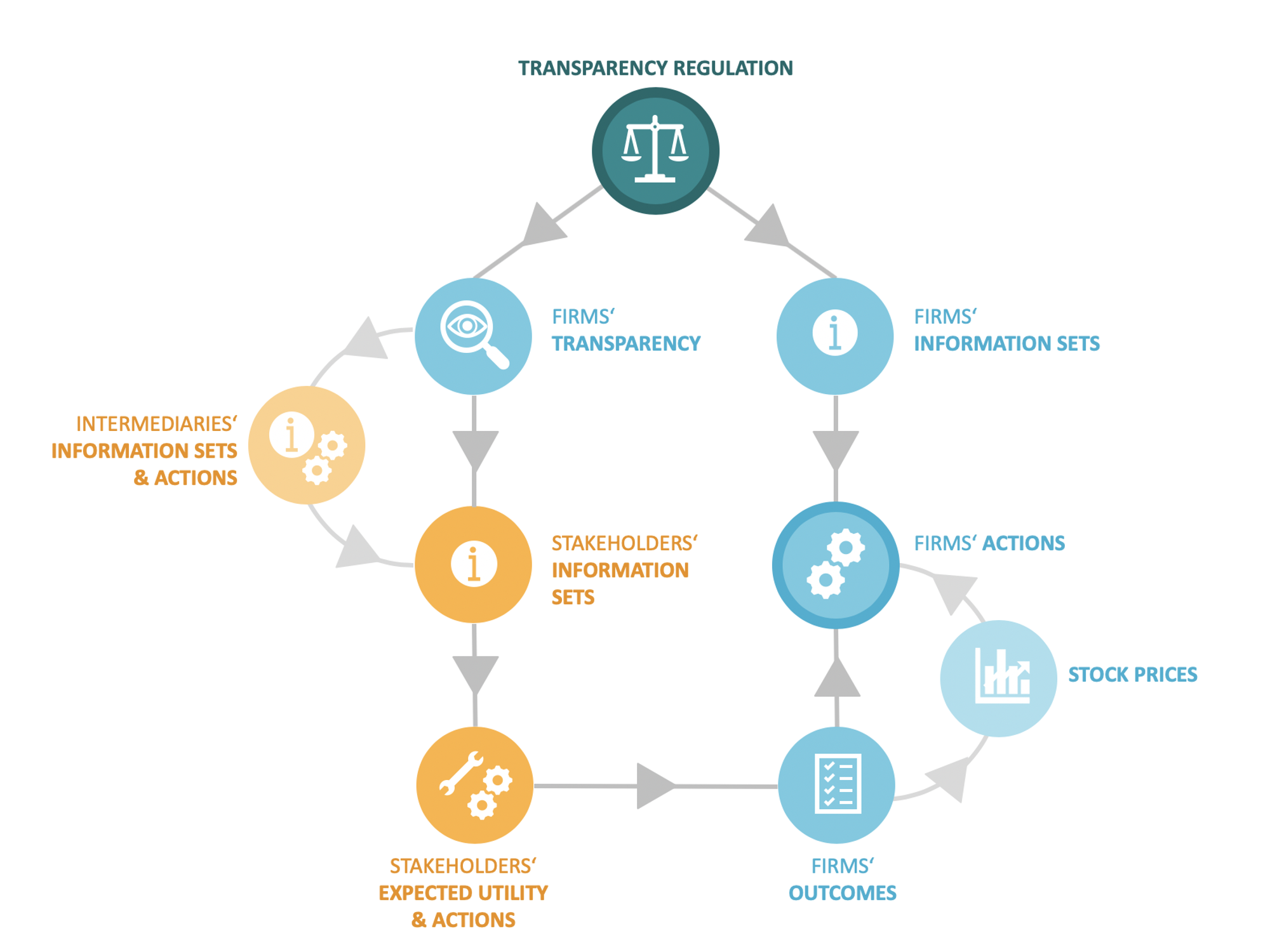

We explored the mechanisms through which targeted transparency implemented via corporate disclosure regulation can lead to changes in a firm’s actions. More specifically, we present a framework for the necessary conditions under which targeted transparency regulation can be effective. The figure below illustrates this possible causal chain. Starting at the top, we show that the first step is that the targeted transparency regulation has to affect the firm’s actual transparency, meaning increasing the quantity and quality of publicly disclosed information.

The effect of targeted transparency on corporate actions

If this prerequisite is met, these disclosures will augment the information sets of stakeholders. Stakeholders include investors, employees, customers, suppliers, government authorities, and the public at large. These stakeholders receive their information either directly from the firm or through intermediaries such as analysts, NGOs, the media, or labor unions. Through the increase in the firm’s transparency, the stakeholders now have access to more, and potentially new, information. This may be beneficial to these groups as this information may previously have been too costly to collect, for example information on the firm’s oil and gas exploration activities in conflict zones. In general, the new information can raise stakeholders’ awareness of a firm’s actions, for example through articles in the media or through NGOs.

Stakeholders’ expectations and actions

The increased information impacts stakeholders’ expectations and their actions. Through transactions, for example by purchasing the firm’s products or buying its stocks, stakeholders obtain utility from the firm. Based on the augmented information sets, stakeholders update their beliefs about the expected net utility they are able to obtain, and act accordingly. Interestingly, stakeholders are not only interested in information about their own expected payoffs, but may also consider the firm’s impact on others, such as an environmentally friendly production process. These are aspects that can be equally valuable to (conscious) customers, investors und (future) employees. For example, investors may value green investments, even if these do not increase the firm’s cash flows. These changes in stakeholders’ behavior affect the outcomes of the firm, e.g., its sales and stock price.

Firms’ responses

Finally, the figure illustrates that firms will likely respond to these (anticipated) changes in stakeholder behavior. For example, a mandate to provide CSR disclosure motivates firms to invest more in CSR to attract investors with CSR preferences. Firms may also be affected indirectly because of effects on their transactions in product, labor, and capital markets due to social pressures and reputation concerns (the left side of the framework). An example we came across is that hospitals reduced their charges in response to greater price transparency, simply because they had reputational concerns about perceived overpricing. Finally, targeted transparency regulation may also reinforce managers’ personal motives to act in line with their stakeholders’ preferences. Managers may put more weight on the social consequences of their investments when they know that they have to share this information with all stakeholders instead of just the capital providers. However, in order for this effect to take place, it is important that managers are aware of, and understand, their stakeholders’ preferences. As such, the effect of targeted transparency regulation on firms’ behavior is likely to vary across firms depending on their relations with stakeholders.

Related Content

Evidence-informed accounting standard setting – lessons from corona

How can researchers and standard setters address validity challenges as they work towards more evidence-informed standard setting?

Read more

Responses