Tax Complexity Index: 2024 data is now available

Researchers from the TRR 266 “Accounting for Transparency” at LMU Munich and Paderborn University have published the 2024 data of the Tax Complexity Index.

With now five waves available (2016, 2018, 2020, 2022, 2024), the Index offers valuable insights into the evolving and increasingly complex global tax landscape for multinational corporations (MNCs). The data is openly accessible on the interactive website: www.taxcomplexity.org.

In recent years, MNCs have faced growing tax complexity, making this an increasingly important area of consideration. This trend is driven by various factors shaping global tax systems, such as new regulations (e. g. the global minimum tax), digitalization, and global tax competition, each of them with potentially ambivalent effects on tax complexity.

The Tax Complexity Index, developed by TRR 266 researchers, measures the complexity of a country’s corporate income tax system as faced by MNCs. It is based on the Global MNC Tax Complexity Survey, which is conducted every two years since 2016. Up to 1,000 tax consultants from up to 110 countries participate in each wave.

Key findings from the 2024 data:

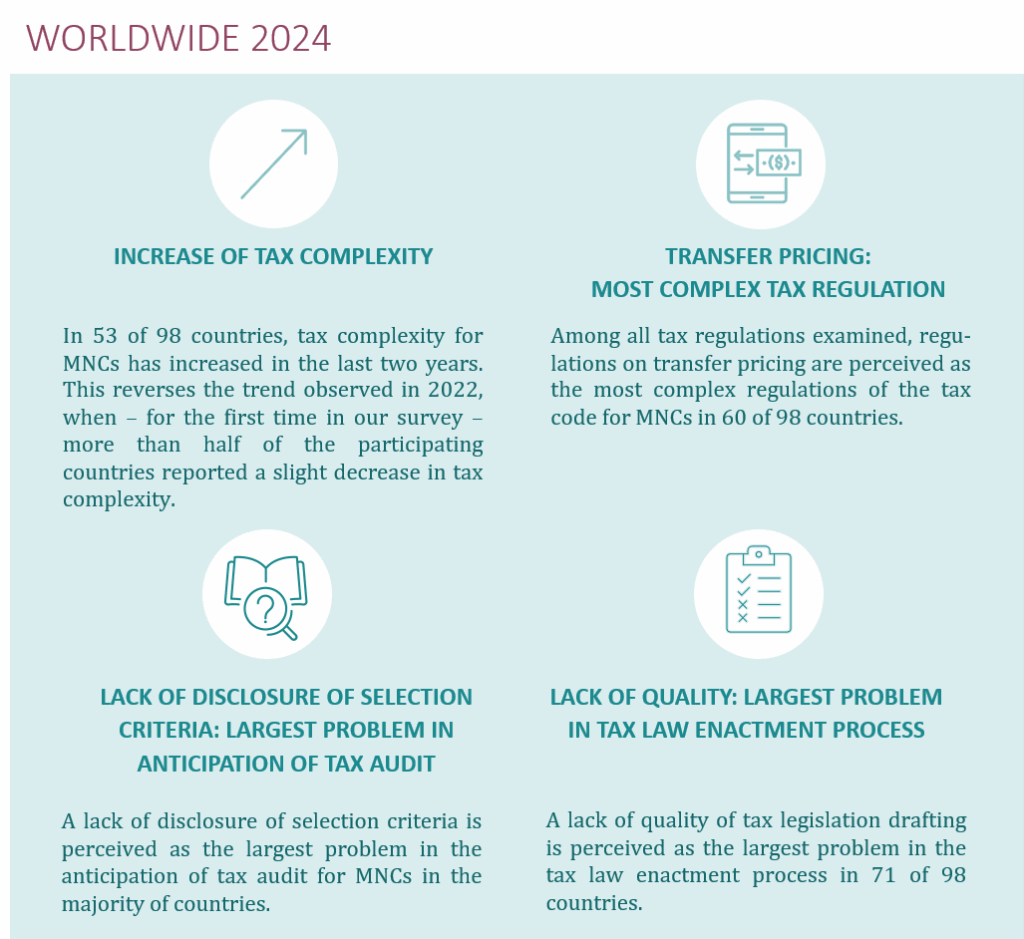

- The 2024 data shows that the general level of tax complexity has increased again over the last two years. Since the start of the study in 2016, it has continually risen every two years except for 2022, where it temporarily remained steady.

- The findings identified transfer pricing rules once again as the most complex tax regulation.

- The surveyed tax experts report that MNC are particularly challenged by the lack of transparency regarding tax audit selection criteria, which makes adequate preparation difficult.

- Regarding tax law enactment, the survey highlights ongoing issues with the quality of tax legislation. Contributing factors include poorly drafted laws, overly complicated language, and inaccurate translations, making the tax code difficult to use for both MNCs and tax administrations.

Focus on OECD countries:

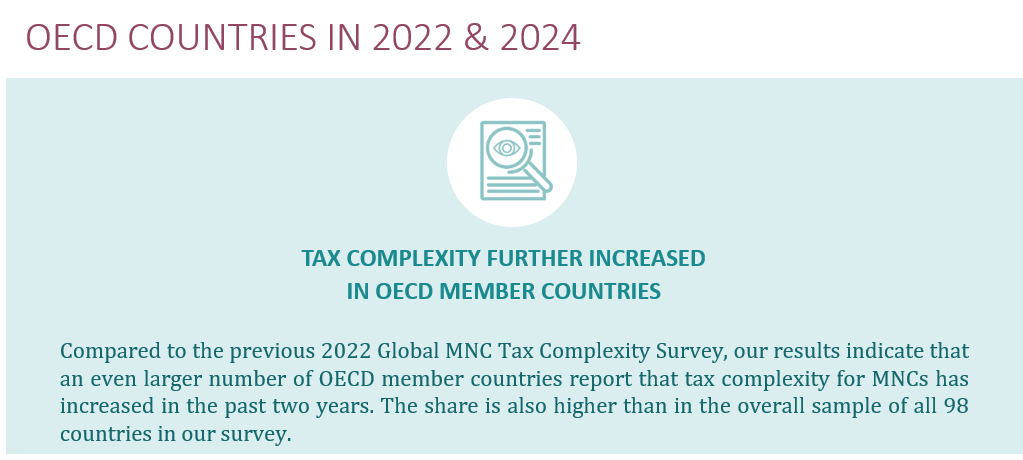

Looking at the OECD countries, the past two years have been marked by significant uncertainty in international tax policy. While, for instance, an agreement on Pillar 2 was reached at EU level at the end of 2022, global implementation has since faced delays and inconsistencies. Several major economies have yet to adopt the minimum tax rules, resulting in ongoing legal and administrative uncertainty in many OECD countries.

This uncertainty is reflected in our results: compared to 2022 respondents from an even larger number of OECD member countries report that tax complexity for MNCs has increased. In addition, respondents in a larger proportion of OECD countries state that tax complexity has primarily negative implications and may influence decisions to relocate business activities abroad.

Detailed information and analyses of the results can be found in the Executive Summary of the 2024 survey and on our Global MNC Tax Complexity Survey webpage.

Interactive website

The newly collected data went through a comprehensive validation procedure and is now openly available on the interactive website. The results are particularly interesting for policymakers, practitioners and researchers. With the data and our analyses, we want to enhance the understanding of tax complexity in and across countries as well as developments over time. In addition to comparing individual countries, the website also offers a comparison of EU and OECD countries.