How Do Firms Rate the CRSD/ESG Reporting Standards? And How Do They Implement Them?

The Corporate Sustainability Reporting Directive (CSRD), introduced in 2023, requires companies in the EU to report comprehensively on their sustainability strategy, environmental and social impacts, and governance structures. Since 2024, it is mandatory for many companies to report according to the CSRD. The regulation is based on the twelve European Sustainability Reporting Standards (ESRS), which are intended to create a uniform framework for ESG (Environmental, Social, Governance) reporting. The aim is to increase transparency for investors, politicians, and society and to make sustainable business practices measurable. But can the guidelines deliver what they promise? TRR 266 research provides insights into the corporate world: What do firms think of the CSRD directive? How do they implement the guidelines? And can the CSRD really achieve greater transparency in reporting?

In this video, TRR 266 researcher Yuhan Liu explains what the CSRD and ESRS are, which companies have to report and what kind of challenges they might face.

How do companies rate the CRSD/ESG reporting standards?

The ESRS guidelines, which aim to standardize sustainability reporting across Europe, are an ambitious goal. However, what sounds good on paper has increasingly been criticized in practice. Feedback from German companies has been predominantly critical. Research findings from the German Business Panel confirm this.

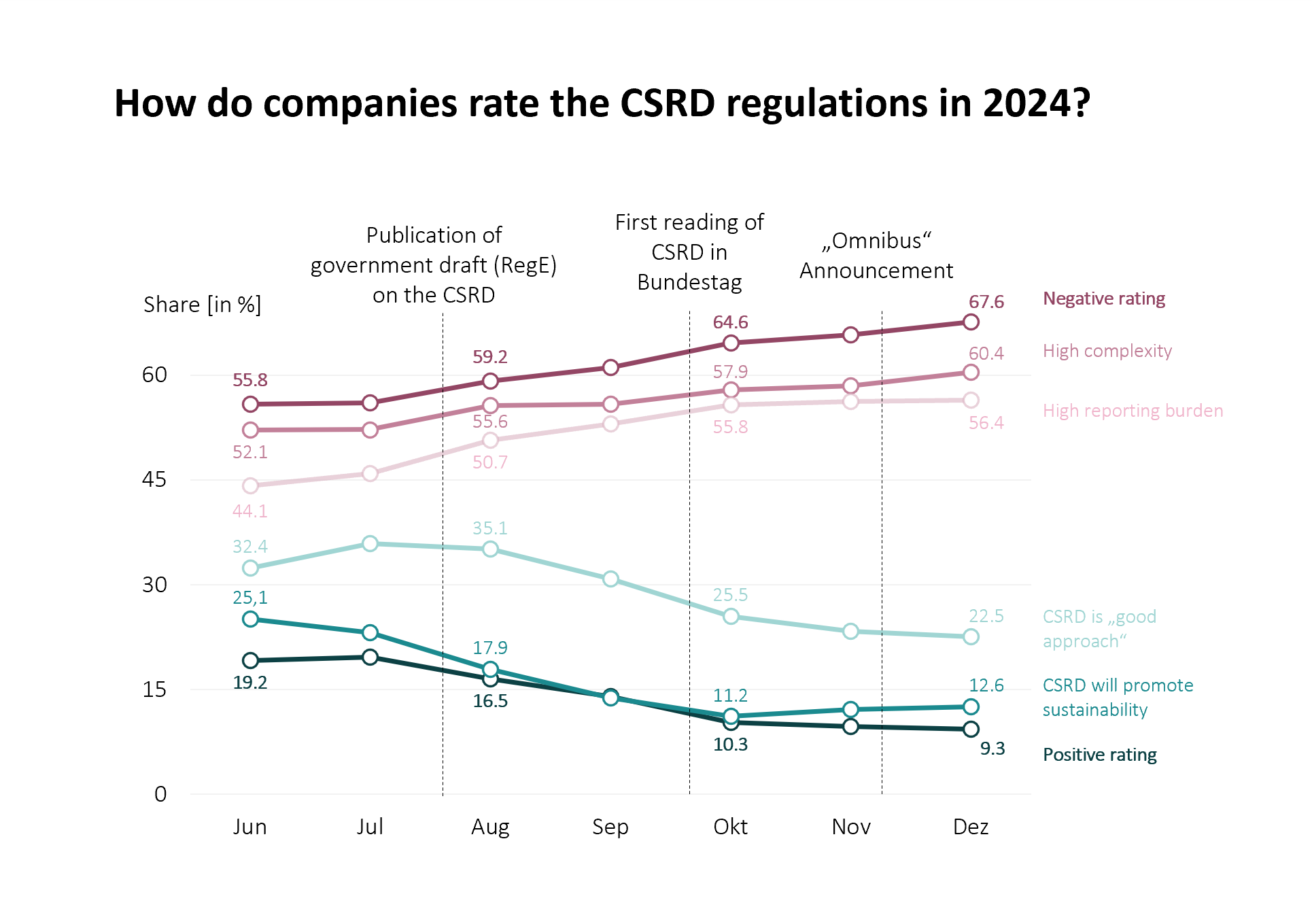

Companies are growing increasingly critical of the CSRD

The attitude of German companies toward the CSRD has become increasingly negative over the course of 2024. At the end of 2024, almost 67.6 percent of companies rated the new reporting rules negatively and only 9.3 percent positively. They particularly criticize the complex and overly detailed standards and the high reporting burden. Only 12.6 percent of companies still believe that the CSRD actually promotes sustainability.

Even sustainability-oriented companies are voicing strong criticism, as considerable resources are being shifted from investments in sustainability projects to pure reporting obligations. The high bureaucratic burden has also led to more than half of all companies surveyed canceling planned investments. Small and medium-sized enterprises (SMEs) are particularly affected by this, as they often lack expertise and personnel in the area of sustainability reporting. Even companies that already operate sustainably often find themselves slowed down by reporting requirements. They rarely see any real added value for internal management or corporate strategy. Instead, companies believe that the main benefit of the ESRS is often reduced to compliance with regulatory requirements.

Regulators should therefore simplify and prioritize CSRD reporting requirements so that companies, especially SMEs, are not overburdened by bureaucracy. The focus should be on actual sustainability results rather than formal aspects. Digital interfaces and leaner administrative processes could help to ensure that implementation is efficient and practical.

Related publications:

Easing reporting requirements leads to greater satisfaction among companies. Need for further reforms remains.

On 16 December 2025, the European Parliament approved the amendments to the Corporate Sustainability Reporting Directive (CSRD) proposed under the so-called Omnibus Initiative – even before the original provisions had been transposed into national law in Germany. In future, only companies with at least 1,000 employees and a net annual turnover of more than €450 million will be required to prepare sustainability reports. In addition, the so-called “stop-the-clock” rule postpones the start of initial reporting obligation by two years for companies that continue to fall within the scope of the CSRD.

This adjustment has been met with widespread approval among German companies. According to the GBP report from January 2026, over 50 percent of the companies surveyed rate the reform positively, primarily because of the expected reduction in bureaucracy. However, some companies express concerns that companies voluntarily opt for a sustainable business model may lose relative competitiveness as a result of the reform.

For many, the reform does not go far enough: over a third of medium-sized and large companies are calling for further simplification and clearer and more reliable guidelines. Many companies devote considerable resources to clarifying exactly what needs to be reported and what the authorities specifically expect. In addition, companies that perceive reporting requirements as bureaucracy invest less in innovation and relocate more production abroad.

Related Publication:

Contact the researchers:

How are companies implementing the CSRD?

Are companies well prepared for reporting, and in which areas do they need support? Several studies from TRR 266 provide insight into how companies are implementing the CSRD.

Smaller and unlisted companies need additional support

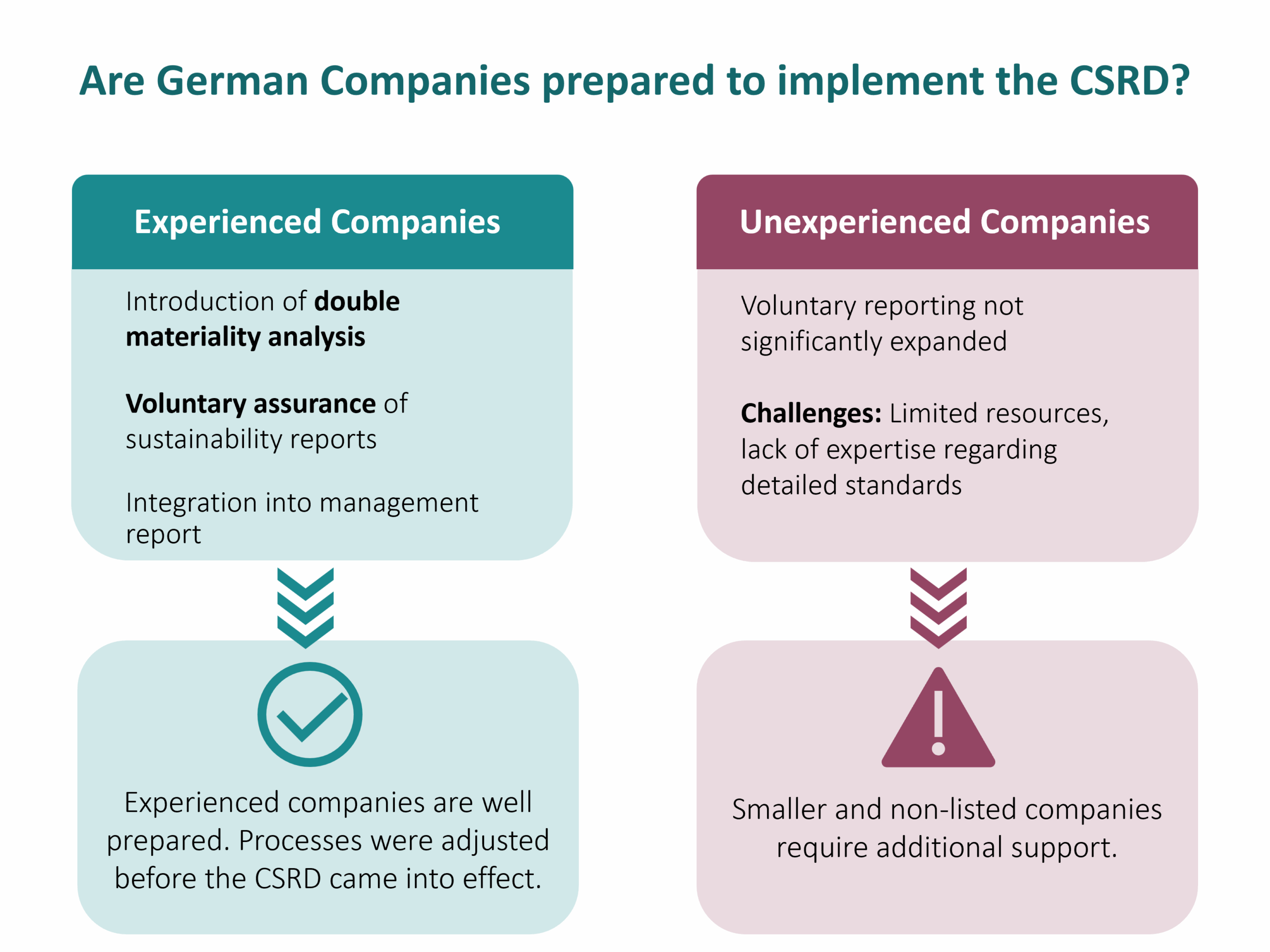

A study from 2024 shows that German companies have prepared for mandatory reporting under the CSRD in different ways, depending on their previous experience. Large companies that are already subject to the Non-Financial Reporting Directive (NFRD), the less comprehensive predecessor to the CSRD, began improving their disclosure practices at an early stage. They are introducing double materiality analyses to identify the most important sustainability issues for a company. They are also seeking voluntary audits of their sustainability reports and increasingly integrating sustainability information into their management reports. These steps show that they have already adapted their processes to the upcoming European sustainability reporting standards ahead of the first mandatory CSRD reporting in 2024. In contrast, many companies that will be subject to the CSRD for the first time have not significantly expanded their voluntary reporting. Limited resources, a lack of expertise, and uncertainty about detailed standards have slowed down their preparations. This suggests that smaller and unlisted companies will need additional support to meet the new requirements.

Related publication:

Contact the researcher:

The first sustainability reports: greater transparency and comparability with room for improvement

In 2025, the first wave of CSRD reports was published for the financial year of 2024. Even though national implementation of the law is still pending, the vast majority of DAX40 companies published CSRD-compliant reports. Researchers at the Sustainability Reporting Navigator (SRN) analyzed these reports and benchmarked DAX40 companies’ 2024 reporting against their 2023 sustainability reports as well as financial reporting.

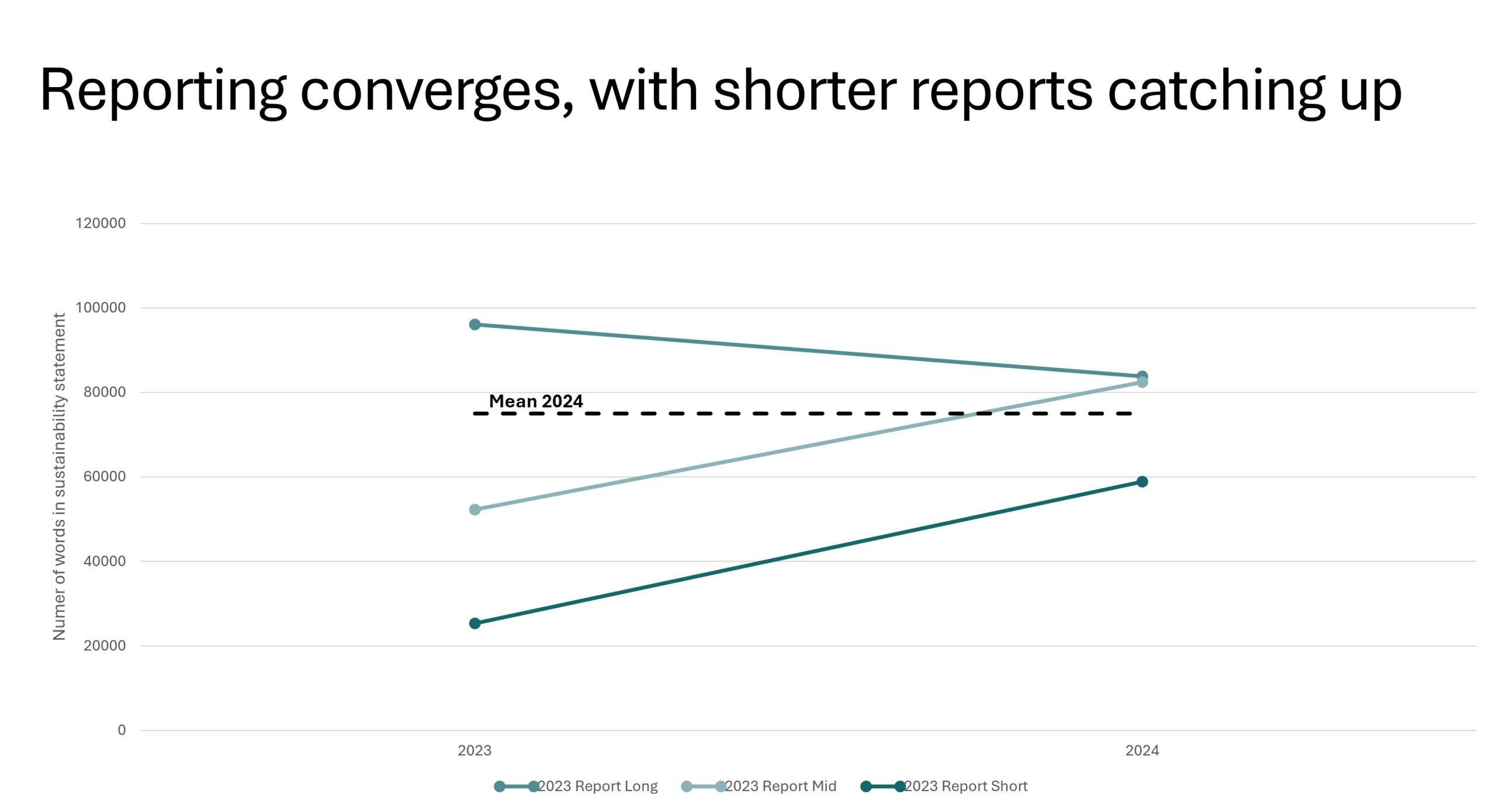

The first applications of the ESRS in the DAX40 show: Sustainability reporting volume (in terms of page and word count) increases, on average. Behind this average increase is a trend toward convergence in firms’ reporting, with short reports becoming longer and very long reports becoming shorter.

But even after this convergence, striking differences between companies persist. Among the DAX40 companies, sustainability reporting volumes ranged from less than 40,000 to more than 140,000 words. In particular, companies differed in terms of the topic they covered in their reports as an outcome of their double-materiality assessment – a key implementation choice under ESRS.

The researchers also looked at the content of DAX40 companies’ first CSRD reports. Compared to the 2023 reporting period, they found a drastic increase in the number of images in the reports, much more standardized language as well as a greater emphasis on negative (compared to positive) words. Taken together, these changes suggest that under the CSRD, companies’ sustainability reporting became a more serious and regulated reporting instrument, on par with companies’ financial reporting.

Materiality Analysis as a Strategic Leverage Point: Interview with TRR 266 Researcher Thorsten Sellhorn

Related content:

Contact the researchers:

Information for Regulators

The CSRD aims at increasing transparency about firms’ sustainability, thereby directing capital flows towards more sustainable investments. Descriptive evidence on firms’ implementation of the CSRD is an important first step in assessing how effective the directive is in achieving this goal. Findings of the TRR 266 suggest that reporting volumes have increased under the CSRD but have also highlighted substantial heterogeneity in how companies implement the new reporting requirements. With our research, we aim to support companies in better understanding reporting market practices, allowing for benchmarking of their own reporting. In our ongoing projects, we will keep monitoring current policy debates and increase our understanding of the interplay between regulatory requirements and companies’ voluntary reporting incentives.

Further information on these pages: