Why ESG Reporting?

Why ESG Reporting?

Extreme weather events, social tensions, economic uncertainty – these developments have the potential to permanently reshape our way of life. About time we pull the emergency brake. But how? One approach that has gained significant traction in recent years is sustainability reporting.

Sustainability reporting aims to reveal how seriously companies take their environmental and social responsibilities – and, by doing so, encourage more sustainable business practices. After all, those who fail to meet rising expectations in these areas risk losing credibility and falling behind more forward-thinking competitors.

Reliable sustainability information is also a key prerequisite for effective policy intervention. Regulations – such as taxes, binding standards, and threshold values – as well as market-based instruments operating through prices and economic incentives, can only be effective if it is transparent how sustainably companies actually operate.

Such transparency enables environmental performance to be compared, helps prevent misaligned incentives, and supports the design of effective governance mechanisms. Reliable measurement and disclosure of metrics such as emissions, resource use or social impacts are essential for monitoring compliance, accurately determining levies, and setting price signals that promote more sustainable corporate practices. Without verifiable and comparable data, neither fair regulation nor effective market steering is possible.

Further reading:

What Mandatory Reporting could achieve

A recent study highlights the significant potential of mandatory

reporting as a catalyst for effective climate policy:

Corporate Emissions Carry a Heavy Price. Transparency could Inform Effective Climate Policy

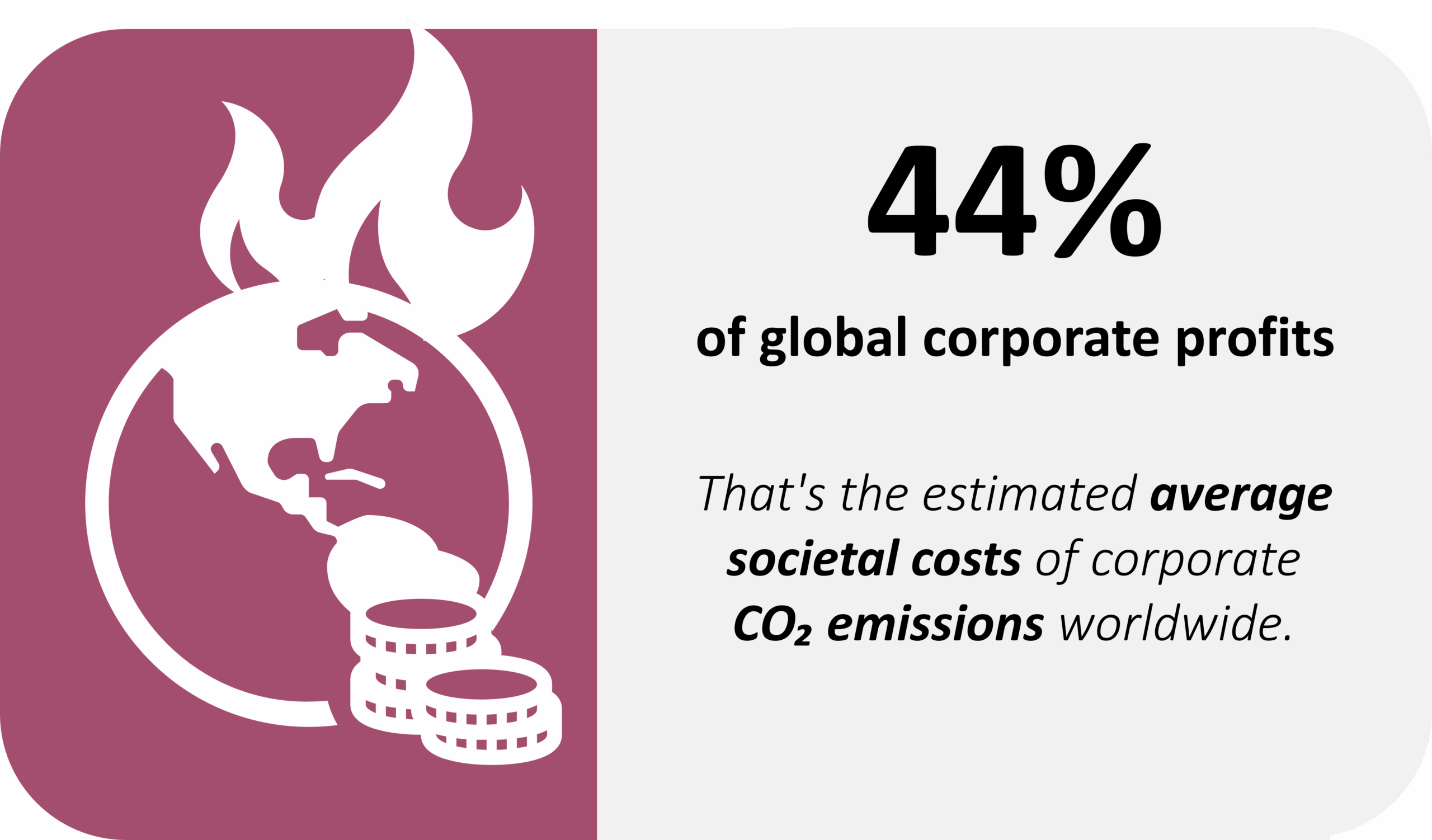

A recent global study estimates that, on average, the social costs of CO₂ emissions from corporate activities amount to 44 percent of firms’ operating profits. The researchers calculated these so-called Corporate Carbon Damages using data from 15,000 publicly traded firms across the globe. At the global scale, the total damages could amount to trillions of U.S. dollars. But responsibility doesn’t rest with companies alone. Consumers also share in this responsibility, for instance through their purchasing decisions, which lead to demand for carbon-intensive goods and services.

The study’s findings not only show that damages are large but also that a small number of companies are responsible for a disproportionate share of them. The 10 percent of firms with the highest corporate carbon damages account for damages equal to 85 percent of their corporate profits. Differences across industries are also striking. Energy, transport, materials, and utilities make up 89 percent of global corporate carbon damages. And even within the same narrowly defined industry, damages vary widely – some companies contribute significantly more damages than their peers.

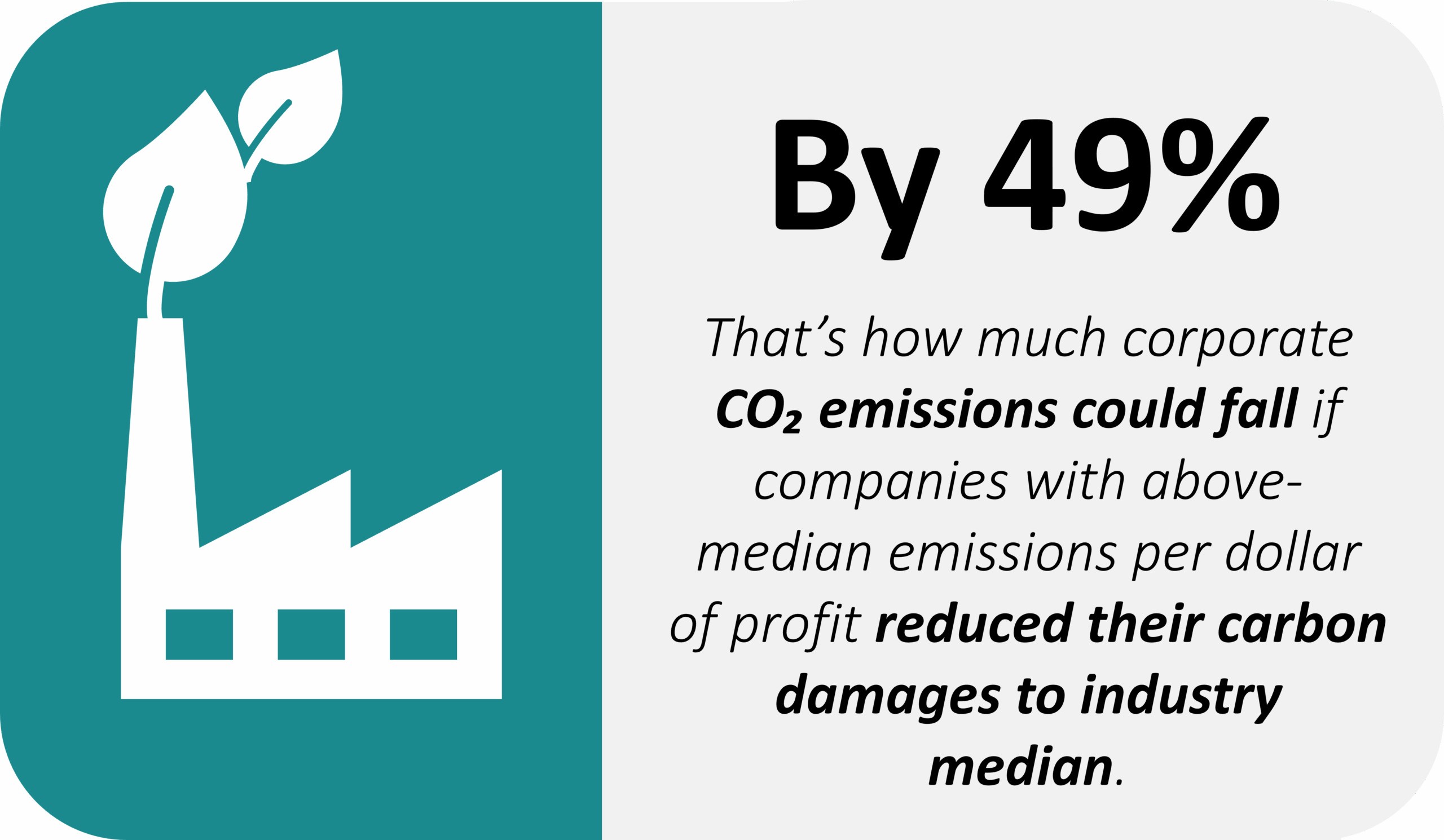

This variation across peers is a major opportunity. If all firms with carbon damages above their industry’s median were to reduce their carbon damages to their respective industry median, total emissions could fall by as much as 49 percent. A dramatic reduction for which mandatory reporting could be the catalyst.

Mandatory disclosure would provide the data necessary for efficient climate policies and market signals, as well as possibly increase pressure on companies to reduce emissions. Sustainability reporting puts corporate climate performance in the spotlight – making differences between companies visible. Firms that lag significantly behind more sustainable competitors face mounting public pressure – from investors, customers, regulators, and the public. This growing scrutiny strengthens the incentive to follow the lead of climate frontrunners in order to stay competitive.

This is what mandatory sustainability reporting could achieve:

Further information:

Read the press release:

Contact the researcher:

Voluntary corporate incentives often

fall short:

Voluntary Disclosure – Truthful Reporting or Strategic Calculation?

More and more companies are voluntarily disclosing sustainability information – often with a clear strategic intent. For many, it’s about gaining favor with investors, appealing to customers, and standing out in the talent market. But which companies are leading the way? And what really drives them? Are their disclosures genuine reflections of corporate values? Are companies taking real action, or merely yielding to increasing stakeholder pressure by overstating their commitment to environmental and social sustainability? Is voluntary reporting enough? Or is there a growing need for binding, standardized disclosure requirements?

Disclaimer:

Providing smoking-gun evidence of greenwashing or the potential shortcomings of voluntary corporate disclosures is challenging, as researchers usually cannot directly observe companies’ actual sustainability activities unless they are disclosed. As a result, it is often difficult to determine with certainty whether the reported information reflects real operational practices or primarily serves communication and self-presentation. The studies featured in this section are therefore subject to certain limitations. Further details can be found in the publications linked throughout the texts.

Biodiversity Disclosures Are Growing Rapidly, but Still Lag Behind Climate Disclosures

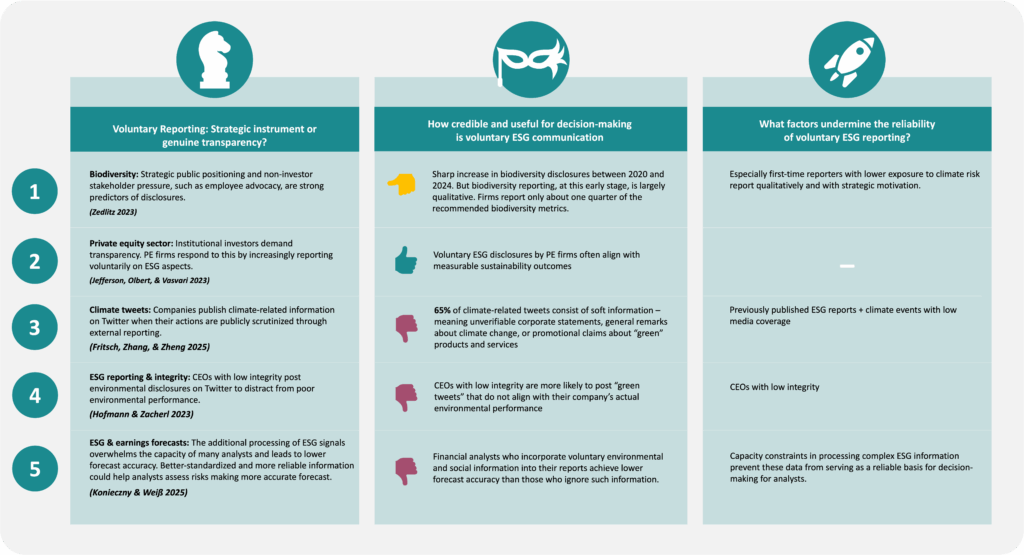

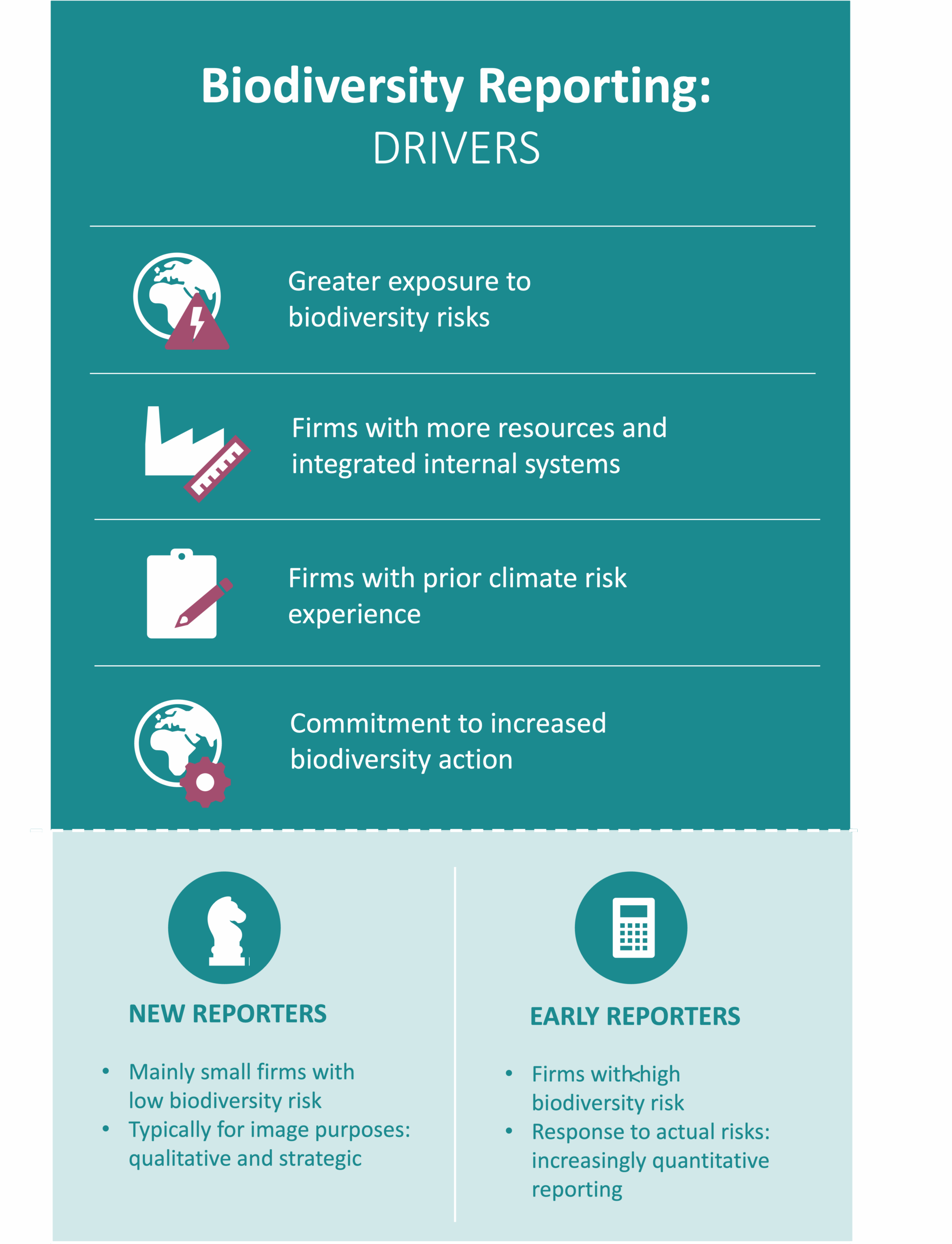

As biodiversity risks are increasingly recognized as financial risks, firms have begun to reflect them in their disclosures. Recent evidence shows a sharp rise in biodiversity reporting among European public firms between 2020 and 2024. During this period, the number of firms recognizing biodiversity risks as financially material increased by about 68%, while the amount of disclosure content more than doubled. This rapid growth reflects a broader shift in how companies perceive biodiversity, moving it from a peripheral sustainability topic toward a more structured risk consideration.

Several factors appear to drive this development. Firms that already possess established capabilities in risk and sustainability reporting are better positioned to incorporate biodiversity risks into their disclosures. In addition, biodiversity reporting appears to benefit from synergies with climate reporting, as firms can draw on existing climate-related reporting frameworks and processes. Pressure from non-investor stakeholders, such as employees or civil society, also plays an important role in encouraging companies to address biodiversity risks in their reporting. In contrast, direct pressure from investors appears to have only a limited influence so far.

Despite the strong increase in reporting activity, biodiversity disclosures still remain less developed than climate disclosures. In particular, firms provide substantially less quantitative information on biodiversity risks, targets, and performance indicators. This difference can be explained by several factors. First, biodiversity reporting is still at an earlier stage of development compared with climate reporting. Second, companies often perceive biodiversity risks as less financially material than climate risks. Third, biodiversity impacts are more difficult to measure and translate into metrics and KPIs.

Overall, the rapid expansion of biodiversity disclosures illustrates how quickly corporate reporting can evolve once new risks are widely recognized. When firms can rely on existing reporting capabilities and build on related disclosure areas, the diffusion of new reporting practices can accelerate considerably.

Read the study:

Contact the researcher:

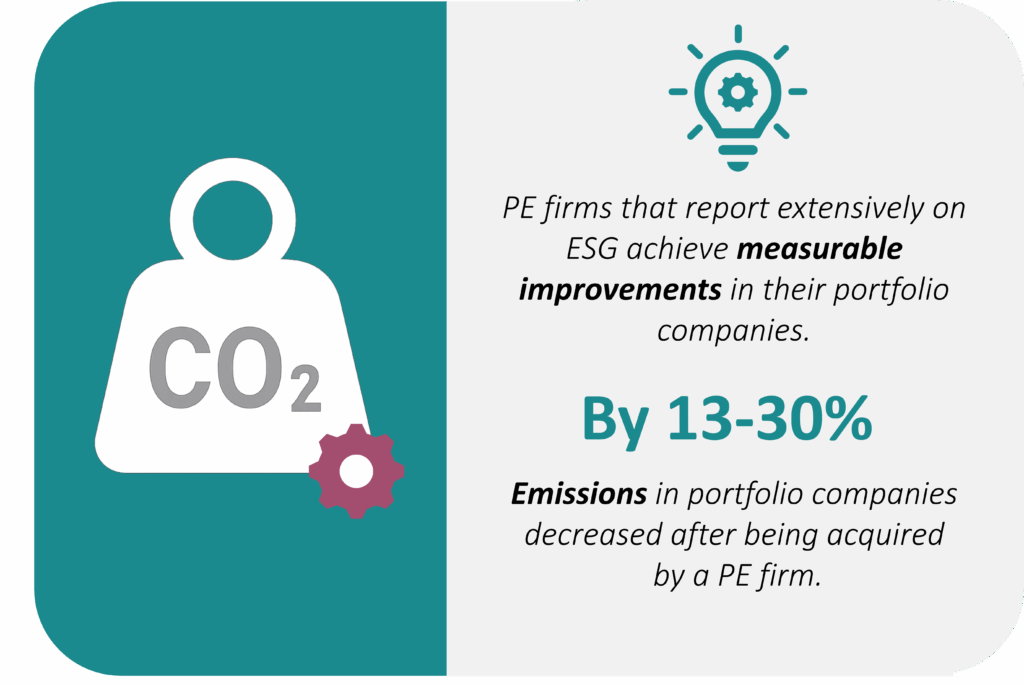

Private Equity Under Investor Pressure: Shadow Market with a Green Coating – or Real Change?

Private equity (PE) firms – investment companies that specialize in investing in non-listed companies – have long operated outside the spotlight of regulatory scrutiny. Unlike their public counterparts, both PE firms and their portfolio companies are subject to minimal mandatory disclosure requirements. This opacity has prompted growing concern among regulators, who are increasingly considering ESG disclosure mandates to guard against the risk of greenwashing. But a recent study shows: the pressure to disclose is growing. PE firms are increasingly publishing ESG information voluntarily.

At the heart of the shift are institutional investors (Limited Partners, or LPs), who are placing greater emphasis on sustainability criteria in their investment decisions. But are these voluntary ESG reports credible? Or is greenwashing still a serious concern within the private equity landscape?

The study offers a revealing insight: PE firms that report extensively on ESG topics also tend to implement corresponding strategies in their investments. In fact, after being acquired by PE firms, portfolio companies experienced emissions reductions of between 13% and 30%, alongside improvements in social performance. In other words, voluntary ESG disclosures by PE firms often align with measurable sustainability outcomes. While the possibility of greenwashing cannot be entirely dismissed, the study suggests that under sufficient investor pressure, even voluntary reporting can drive real-world impact.

Still, this is far from a case against mandatory disclosure. PE firms whose investors are based in countries with extensive ESG regulation show significantly higher levels of voluntary ESG disclosure. In this way, public market disclosure rules spill over into private markets, as investors transfer their expectations.

Read the study:

Contact the researcher:

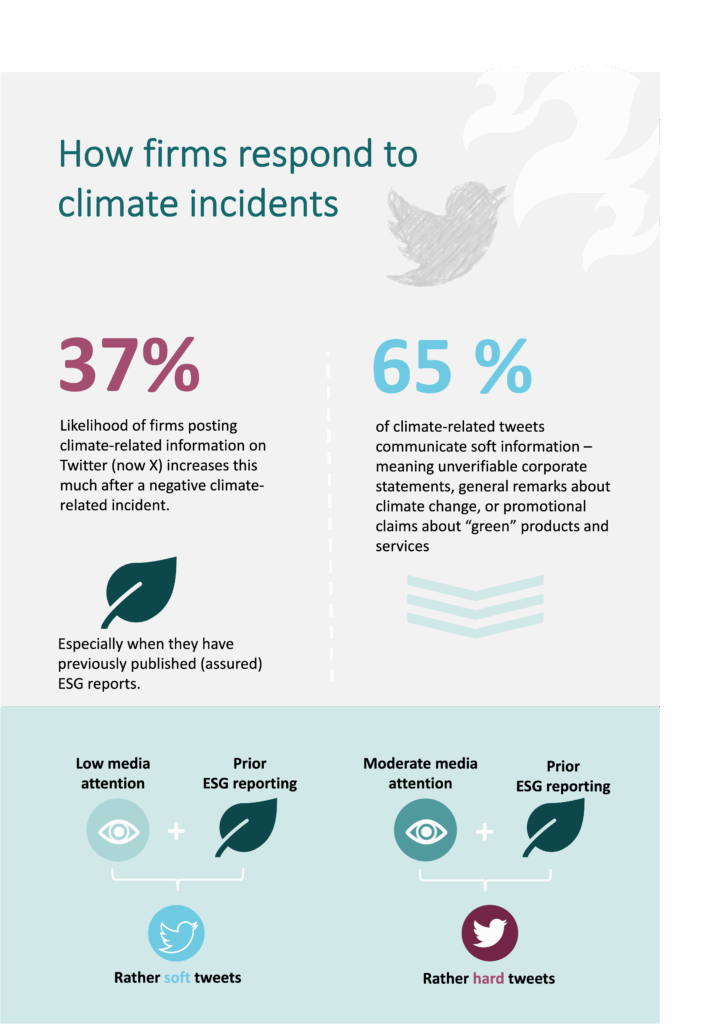

Soft Talk After the Storm: How Companies Navigate Climate Reputation Risks

Companies are most likely to voluntarily disclose climate-related information when their actions are publicly scrutinized through external reporting. That’s the finding of a recent study examining how firms respond to negative media coverage – specifically on Twitter (now X).

The data show that following a negative climate-related incident, companies are 37 percent more likely to publish climate-relevant information on the platform. This effect is especially pronounced when companies have previously published ESG reports — particularly when those reports have been assured.

However, this type of disclosure is prone to greenwashing. According to the study, 65 percent of climate-related tweets consist of soft information – meaning unverifiable corporate statements, general remarks about climate change, or promotional claims about “green” products and services. Whether companies respond to negative climate events with soft or hard information is a strategic decision, in which they weigh their reputation against the severity of the incident.

A key factor in this decision is whether the company has previously published ESG reports. If companies have already built a strong reputation through prior ESG reporting, they tend to respond to climate incidents with low media attention with soft climate tweets – vague or promotional messaging that avoids scrutiny. In contrast, when the media attention is moderate, they are more likely to issue hard climate tweets, offering verifiable and substantive claims in order to meet heightened stakeholder expectations – particularly if their ESG reports have been assured.

Overall, assured ESG reports are more closely associated with the disclosure of hard facts than unassured ones. This suggests that verification strengthens a company’s commitment to substantive, consistent communication. Voluntary ESG disclosures are, by nature, strategic – and therefore vulnerable to cheap talk and greenwashing. However, assured ESG reports, in particular, can help discipline and improve the quality of voluntary disclosures.

Read the study:

Contact the researchers:

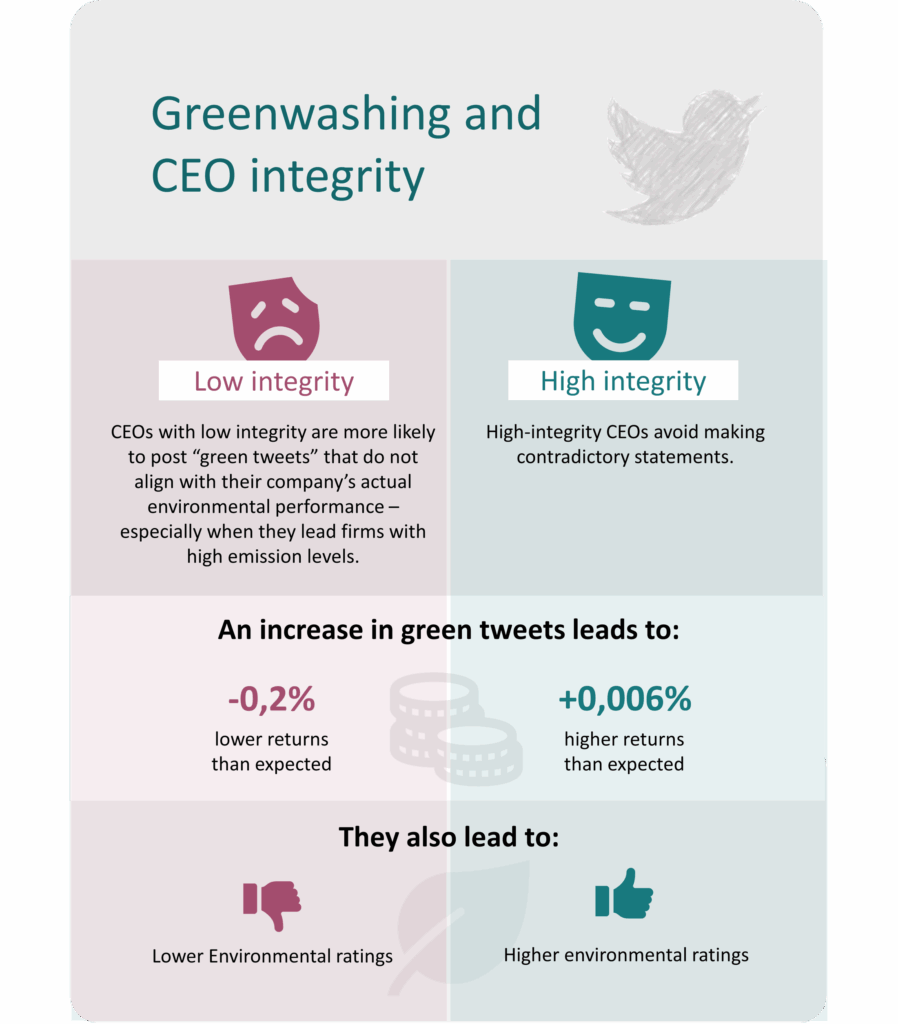

Greenwashing Starts at the Top: How CEO Integrity Shapes ESG Communication

Whether companies report their ESG performance truthfully depends largely on the personal integrity of their CEOs. That’s the finding of a recent study examining voluntary ESG disclosures

via Twitter (now X).

According to the study, CEOs with low integrity are more likely to use voluntary environmental messaging on Twitter to distract from poor environmental performance. They post more “green tweets” that do not align with their company’s actual environmental performance – especially when they lead firms with high emission levels. In contrast, high-integrity CEOs avoid making contradictory statements. For them, the reputational cost of engaging in questionable disclosure practices is simply too high.

However, investors and analysts are not easily fooled by this form of greenwashing – leading to significant consequences for the company involved. When a low-integrity CEO suddenly increases the volume of green tweets, the company’s returns tend to perform worse than initially expected. An increase in green tweets of one standard deviation involves a reduction in abnormal returns by 0.2 percent. For trustworthy CEOs, the opposite is true: returns develop 0.006 percent better than expected. In other words, investors place greater trust in CEOs with high integrity.

The same pattern holds true for environmental ratings by ESG analysts. When untrustworthy CEOs publish a high number of green tweets, their companies tend to receive lower ratings. In contrast, firms led by trustworthy CEOs see their environmental scores improve as their ESG messaging increases.

Guidance for Regulators

The study sends a clear message: greenwashing is also a matter of leadership ethics. Making ESG disclosures mandatory and standardized would significantly reduce the opportunity for low-integrity CEOs to manipulate public perception through selective or misleading green messaging on platforms like Twitter.

Read the study:

Contact the researcher:

More Effort, Less Precision: How Environmental and Social Data Undermines Analysts’ Forecast Accuracy

Sustainability information is meant to provide guidance and improve forecast accuracy. But a recent study shows it doesn’t always work that way. Analysts who include environmental or social information (E and S) in their reports are on average less accurate than their peers who exclude such information. On average, forecasters who consider environmental data are 5.6% less accurate compared to their peers, while those using social data are 2.6% less accurate.

The findings suggest that processing an additional ESG signal alongside traditional financial information overwhelms the capacity of many analysts. The effect is especially pronounced for those with large and diverse portfolios. In these cases, the complexity of the information increases cognitive load and makes accurate forecasting more challenging. Analysts from smaller brokerage houses, with less infrastructure, also experience bigger drops in forecast accuracy – even though larger brokerage houses do not necessarily deliver more precise forecasts.

Interestingly, the effect goes beyond forecasts that explicitly use E and S data. Analysts who increasingly rely on environmental and social information also make larger forecast errors for companies where they don’t even draw on such data. Once an analyst consider E&S information for a certain share of companies in their coverage, the average error rate rises noticeably also for the other firms within their portfolio. This points to general negative spill-over effects in processing complex information signals

Finally, the negative effect is most pronounced for analysts with relatively pessimistic forecasts while more optimistic analysts do not show the same pattern. This suggests that these pessimistic analysts may overestimate E and S risks, which could explain why they experience a lower forecast accuracy compared to their peers who exclude such information.

Implications for Regulators

The findings make a strong case for mandatory ESG reporting with more and clearer standards, especially on environmental issues like CO₂ reduction and energy efficiency, which are most prone to forecasting errors. Better-standardized and more reliable environmental and social data could help analysts assess risks making more accurate forecasts.

Read the study:

Contact the researcher

Why Mandatory ESG Reporting is Essential

From Optional to Mandatory: Reliable Data, Better Decisions

Sustainability is no longer a fringe concern. Consumers, investors, and employees are increasingly aligning their purchasing, investment, and career choices with environmental and social values. As a result, companies are under mounting pressure not just to communicate their commitment credibly but to demonstrate real progress. Yet in many cases, voluntary sustainability reporting fails to deliver. While it can prompt incremental change — particularly when external scrutiny from investors, customers, or the public is high — academic research has repeatedly underscored its flaws. Voluntary ESG reports are often selective, shaped by strategic interests, and difficult to compare across firms. What’s lacking is reliable, verifiable information on how companies actually perform when it comes to sustainability.

This is precisely where mandatory ESG reporting comes in. By requiring companies to disclose relevant information – even when it may be inconvenient or strategically disadvantageous – it fosters transparency. Ideally, it establishes uniform standards that make ESG performance measurable, comparable, and verifiable.

Beyond enhancing transparency, mandatory reporting can help embed sustainability more deeply into corporate strategy and operations – providing stakeholders with the reliable ESG data they need to make informed decisions. Investors gain a clearer view of long-term risks, consumers can align their purchasing choices with their values, and companies are better equipped to select suppliers based on sustainability criteria. This increases the pressure for meaningful change – guiding companies and markets toward a more environmentally and socially sustainable economy.

But what should these reporting requirements look like to unlock their full potential? Are current regulations fit for purpose? What real impact can they truly have? Can they prevent greenwashing? Are companies embracing them – or merely complying? How can companies be supported in implementing them? And ultimately: Is mandatory reporting enough? Or are additional incentives necessary?

Impact Requires Clarity:

Why Mandatory ESG Reporting Only Works with Binding and Uniform Standards

What does it take for mandatory ESG reporting to actually make a difference? Two studies on previous disclosure regimes show: Without clear standards and defined minimum requirements, even mandatory ESG reporting often remains selective, fails to reflect stakeholder interests or remains incomplete in key areas – such as taxation. Another study offers guidance on how regulatory disclosures should be designed to truly drive sustainable investments. These findings provide crucial insights for the successful implementation of the new EU regulations: With its Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS), the EU aims to make sustainability reporting more consistent, verifiable, and comparable – raising the bar for corporate transparency.

NFRD: Without Binding Standards, Stakeholder Voices Remain Unheard

Between 2017 and 2023, the European Union’s Non-Financial Reporting Directive (NFRD) sought to usher in a new era of corporate transparency by requiring companies to disclose information on environmental and social matters. Yet the initiative, despite its ambition, fell short of ensuring comparability. By granting companies broad discretion and failing to mandate binding reporting standards or metrics, the directive led to wide disparities in how — and what — companies reported, even among entities operating under similar conditions. This is highlighted by a recent study examining to what extent diverse information needs of stakeholders and CSR governance influence the mandatory CSR reporting of German savings banks.

The findings are revealing: CSR reporting is clearly associated with strong CSR governance — reflecting how sustainability is institutionally embedded, organized, and managed within banks. Banks that establish strong CSR governance tend to have longer CSR reports and report more extensively on social issues, human rights and CSR strategy.

To a lesser extent, the political influence of municipalities and interests of bank clients shape CRS reporting. Where representatives of municipalities, such as mayors or county commissioners who chair supervisory boards, belong to a left-wing or Green party, CSR reports tend to be longer and provide more extensive coverage of overall CSR strategy. A higher share of Green party members on the municipal council (as representatives of municipalities) correlates with more extensive reporting on social issues. The sustainability orientation of private clients also exerts some influence. When clients place greater value on sustainability, the coverage of overall CSR strategy increases.

Documented associations between CSR reporting and stakeholders’ interests primarily exist in banks with strong CSR governance. In sum, CSR reporting of savings banks better mirrors the interests of stakeholders when accompanied with establishment of CSR governance.

Guidance for Regulators

These findings point to a broader concern: Even when mandatory reporting frameworks give flexibility and discretion to report relevant information to stakeholders, CSR reporting only partially aligns with stakeholders’ interest. Importantly, an essential driver of better alignment is strong CSR governance.

The results underscore the need for more precise, standardized, and binding reporting requirements as well as promotion of strong CSR governance, ensuring that stakeholder voices are adequately represented.

Until then, the story companies tell about their social and environmental impact will depend very little on interest of stakeholders.

Read the study:

Contact the researcher:

Taxes in ESG Reporting: Fragmented, Inconsistent, and Hard to Find

Taxes are a vital way companies contribute to the common good. They finance essential services like education, healthcare, and social infrastructure. They incentivize environmentally friendly behavior and help fund climate action. As such, taxes serve as a key indicator of corporate social and environmental responsibility. Nevertheless, a recent study on sustainability reports from Germany, France, and Italy reveals: Despite their importance, tax-related sustainability reporting is fragmented, inconsistent, and often hard to find.

On average, companies meet less than 50% of the requirements set out in the GRI 207 standard — a tax reporting standard introduced in 2021 to help implement the EU Non-Financial Reporting Directive (NFRD). However, the standard grants companies considerable leeway in deciding whether and how to disclose tax-related information.

Two principles are particularly important in this context: The “materiality principle” requires companies to disclose all topics with significant economic, environmental, or social impact — but leaves it up to them to decide what is considered as “material.” The “comply-or-explain principle” allows companies to either report or explain why they haven’t reported. This combination often results in tax disclosures falling by the wayside — especially without external audits to enforce transparency. The study casts doubt whether these freedoms are appropriate. Given the critical importance of taxes, the authors argue that tax information should be considered material by default – and thus mandatory under the EU’s Corporate Sustainability Reporting Directive (CSRD) which replaced the NFRD.

The study also exposes a fragmented reporting landscape that differs widely across countries. Tax information appears under varying titles, scattered across different documents, with frequent content gaps and no consistent classification within the ESG pillars of Environment, Social, and Governance. As a result, tax disclosures are often hard to locate, difficult to interpret, and difficult to compare.

Guidance for Regulators

The authors call for clear, standardized requirements on what tax information should be reported, how it should be structured, and where it should be located within the sustainability reporting package — ideally through a dedicated standard within the European Sustainability Reporting Standards (ESRS), anchored in the Governance pillar. Content and presentation must be considered together so that report users — such as investors, tax authorities, and civil society — receive information that is truly understandable and comparable.

Read the study:

Contact the researchers:

When Market Sentiment Moves Capital: What This Means for ESG Disclosure Rules

An increasing number of investors are favoring companies with a positive environmental impact. But it’s not only personal sustainability preferences that shape investment decisions – the belief that other investors prioritize sustainability also plays a critical role, regardless of one’s own values. This is demonstrated by a recent study, which offers important insights for shaping ESG disclosure requirements.

In an experiment, researchers found that investors who believe other investors prioritize sustainability are more likely to invest in sustainable companies – even if their own preferences are less pronounced. However, these decisions aren’t tied to actual ESG performance. That’s only the case for investors with strong pro-sustainability preferences: they invest more when ESG performance is positive and less when it is negative. In essence, beliefs and preferences complement each other, jointly fueling the momentum behind sustainable investing.

A key takeaway for companies and regulators: the format of ESG disclosures – whether narrative or visual – does not measurably affect investment behavior. What matters is the content: those who report on sustainability openly and credibly can attract more capital – not only from dedicated sustainability enthusiasts, but also from those anticipating market trends. For companies, it is therefore worthwhile to invest in strong sustainability performance and transparent communication.

Guidance for Regulators

The study itself stops short of making policy recommendations. Still, its findings invite broader reflections on ESG reporting: To make ESG disclosures more effective, it could be helpful for reports to offer more measurable and comparable sustainability data — for example through standardized frameworks and relevant metrics. Additionally, regulators could consider promoting transparency around market sentiment and expectations, for example through sentiment indicators or benchmarks. This could help guide green investment decisions more effectively.

Read the study:

Contact the researcher: