Tax Complexity Index: 2020 data is now available

Researchers from TRR 266 “Accounting for Transparency” at LMU Munich and Paderborn University publish the 2020 data of the Tax Complexity Index. With now three years available (2016, 2018, 2020), the data offers insights into the development of rapidly changing tax landscapes for MNCs. The data is available via open access on the interactive website www.taxcomplexity.org.

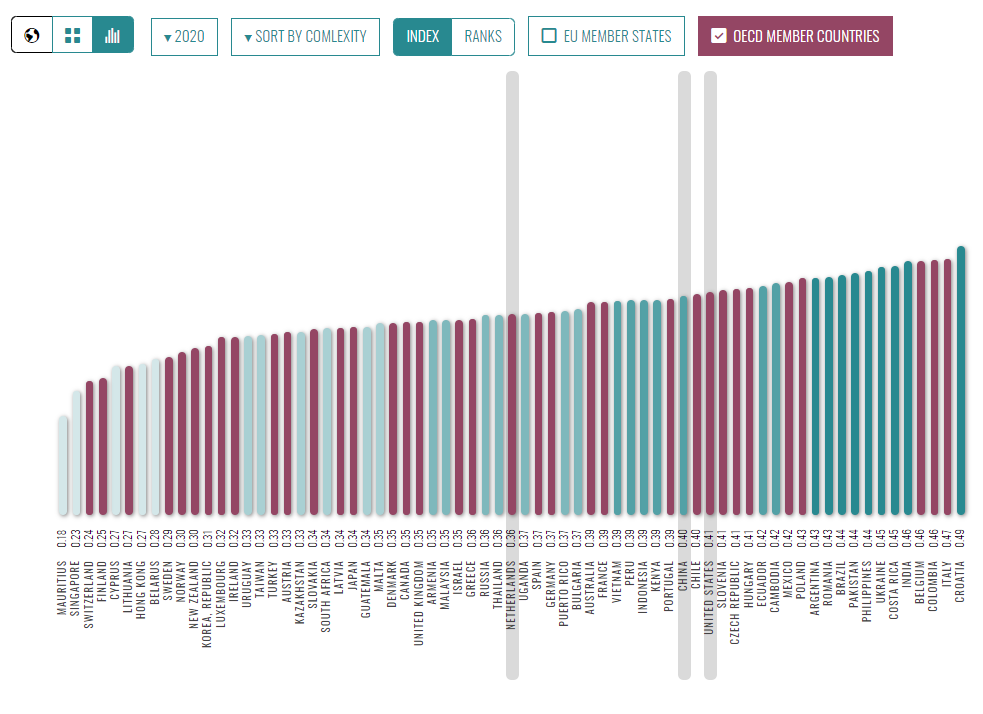

The Tax Complexity Index measures the complexity of a country’s corporate income tax system as faced by multinational corporations and is based on a global survey. Since 2016 the survey is conducted every two years and answered by local tax experts at international tax consulting firms and networks in more than 100 countries. The main findings of the 2020 Global MNC Tax Complexity Survey have once again shown that the general level of tax complexity has increased in the last two years. The findings also identified transfer pricing as the most complex tax regulation and problems in other areas, such as quality defects in enacting new tax laws. Detailed information about the results can be found in the Executive Summary of the 2020 survey.

The newly collected data is now validated and openly available on the interactive website. The website allows interested parties, such as policymakers, practitioners and researchers, to learn more about tax complexity in different countries and to compare the overall tax complexity index of countries over a time frame from 2016 to 2020. In addition to comparing individual countries, the website also offers a comparison of EU and OECD countries.

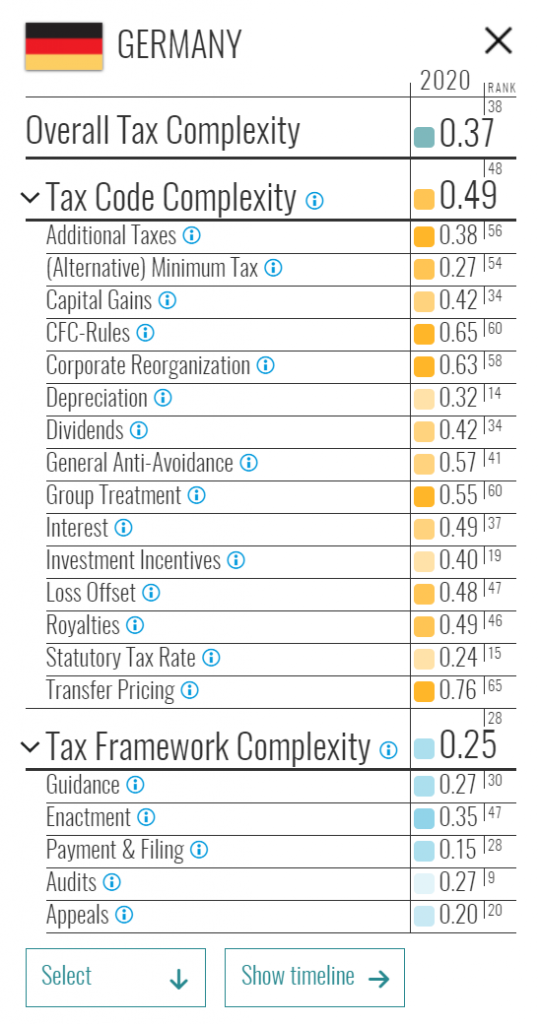

The Tax Complexity Index covers both tax code (i.e. tax regulations) and tax framework (i.e. features and processes of a tax system) complexity. The Tax Complexity Index can be disentangled into individual tax regulations, such as CFC-rules and transfer pricing, and dimensions, such as tax law enactment and tax audits. By selecting a country, a more granular view shows all tax regulations and dimensions, which allows to identify for example the least and most complex regulation in that country. Germany, for instance, has an overall medium tax complexity with a comparably high tax code complexity and low tax framework complexity.

The website also enables users to create their own index to control the effect each individual value has on the overall tax complexity index. This allows users to compare individual countries´ tax complexity, for instance, specifically with respect to the tax regulations for dividends and interest. Finally, users can download their customized Tax Complexity Index.