Using taxes to promote healthy choices: Effective solution or economic burden

Healthcare costs are rising globally due to conditions such as obesity and diabetes. In response, the World Health Organization (WHO) recommends targeted taxes to reduce the consumption of excess sugar. This debate has gained momentum in Germany as well, with the National Academy of Sciences Leopoldina suggesting a general sugar tax on all sugary foods.

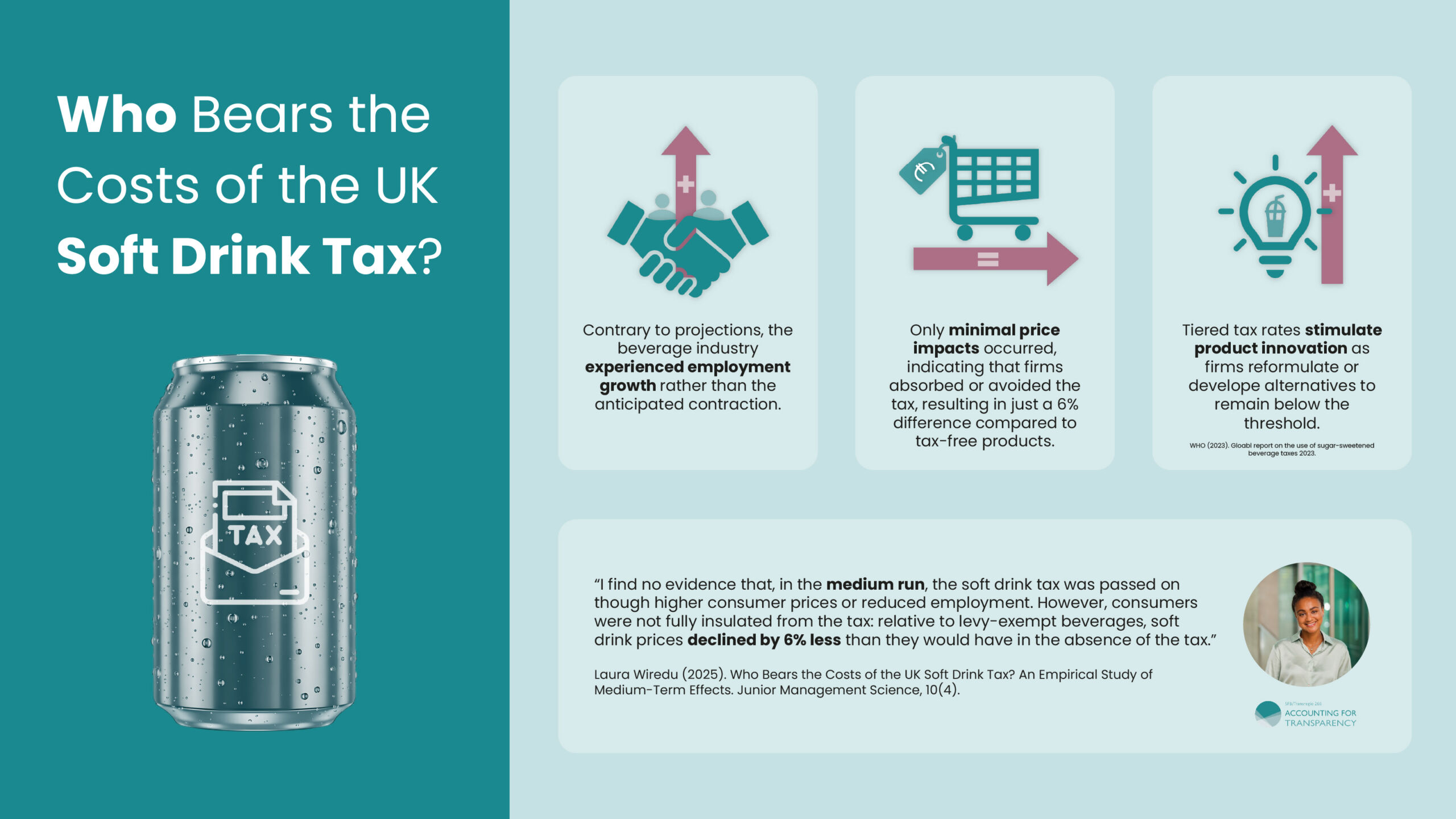

While the health benefits are clear, the discussion is often overshadowed by economic concerns. Critics warn of rising prices for consumers and potential risks to the labor market. This raises a central question: Who actually bears the burden of such a tax?

This is where Laura Wiredu’s research at Universität Paderborn comes in. In her master’s thesis, she examined the medium-term effects of the UK soft drink industry levy in the five-years following its introduction. Her study was recently published in Junior Management Science journal. We are delighted that she is now continuing her academic career as a PhD student within the TRR 266.

Her findings paint a clear picture in the medium run:

𝐔𝐧𝐞𝐱𝐩𝐞𝐜𝐭𝐞𝐝 𝐞𝐦𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭 𝐭𝐫𝐞𝐧𝐝𝐬: There were no negative impacts on the number of employees in the affected firms. In fact, the beverage industry as a whole saw significant employment growth during the period studied.

𝐋𝐨𝐰 𝐛𝐮𝐫𝐝𝐞𝐧 𝐨𝐧 𝐜𝐨𝐧𝐬𝐮𝐦𝐞𝐫𝐬: The tax has had little impact on consumers. As overall beverage prices decreased, soft drink prices fell only 6 % less than those of tax-free products like water or juice. This suggests that manufacturers have absorbed most of the tax instead of passing it on to consumers.

𝐒𝐭𝐢𝐦𝐮𝐥𝐚𝐭𝐢𝐧𝐠 𝐩𝐫𝐨𝐝𝐮𝐜𝐭 𝐢𝐧𝐧𝐨𝐯𝐚𝐭𝐢𝐨𝐧: Tiered tax rates encourage firms to innovate (WHO, 2023). Since the tax was hardly passed on, this indicates that firms either absorbed or mitigated the costs by lowering sugar content to stay below the threshold or by developing sugar-reduced alternatives to avoid the tax.

The research concludes that, under the UK model, the burden of a soft drink tax was not significantly passed on to consumers or employees.

Read the full paper here: https://jums.ub.uni-muenchen.de/JMS/article/view/5330